Company dissolution services in Vietnam 2026 assist enterprises in completing all dissolution procedures, tax settlement, tax code closure, and legal documentation in accordance with the law.

In reality, the enterprise dissolution procedures involve not only submitting dissolution documents but also tax settlement, tax code closure, asset liquidation, and handling various other legal obligations. If not done correctly, the dissolution process can be prolonged, incurring additional costs, or resulting in administrative penalties.

Choosing to cease operations and dissolve a company in Vietnam is never an easy decision for enterprise owners. Besides financial and personnel pressures, many enterprises also face difficulties in handling closure paperwork, dealing with tax authorities, or completing outstanding legal obligations.

Understanding these difficulties, Viet An Law provides comprehensive business dissolution services in 2026, supporting clients from legal consultation, document preparation, dissolution tax settlement to completing procedures at the business registration authority. With a team of experienced lawyers and experts, Viet An Law is committed to assisting enterprises in carrying out procedures quickly, in accordance with regulations, and at optimal costs.

| Criteria | Information |

|---|---|

| Service | Full-package company dissolution services |

| Main procedures | Vietnam company dissolution dossier preparation, tax finalization, and closing of the tax identification number |

| Execution timeline | Approximately 30 – 90 days, depending on the specific status of the corporate dossier |

| Prerequisites for dissolution | The enterprise must have no outstanding debts or unfulfilled financial obligations |

| Critical milestone | Tax finalization for dissolution and closing (deactivating) the corporate tax identification number |

| Processing authorities | Business Registration Office under the Department of Finance |

| Tax obligations | Mandatory to be fully completed and cleared prior to company dissolution |

| Social insurance obligations | Must fully settle social insurance contributions and ensure all employee benefits are resolved |

| Applicable entities | Limited liability companies, Joint stock companies, and FDI enterprises. |

| Service support | Providing corporate dissolution consultancy, handling legal dossiers, and acting as the authorized representative to work with competent state authorities |

Not all business dissolution cases are straightforward. For businesses with outstanding tax obligations, incomplete accounting records, or those with foreign elements, using company dissolution services can help mitigate legal risks, save time, and avoid repeated requests for document revisions.

| Case | Why business dissolution services should be used |

| Enterprises with outstanding tax liabilities | Need to review tax obligations, prepare handling dossiers, and conduct tax finalization prior to dissolution |

| Enterprises with locked tax codes | Must work with the tax authority to restore or resolve the tax code status before submitting the dissolution application dossier |

| Incomplete accounting books and records | Need to supplement supporting documents, complete accounting books, and resolve outstanding accounting and tax issues |

| FDI companies | Must execute additional procedures for terminating the investment project and handle all relevant obligations |

| Lack of dedicated legal or accounting personnel | Difficult to track the dissolution process, application deadlines, and compliance requirements from state authorities |

Many businesses cease operations but have not yet declared or fulfilled their tax obligations. Before dissolving a company, it must settle all outstanding tax debts, late payment penalties, and other financial obligations. This is one of the common reasons why dissolution procedures are prolonged.

In cases where a business’s tax identification number is locked, it is not operating at its registered address, or it is placed in a state of inactivity, dissolution typically requires processing with the tax authorities before the dissolution application can be accepted.

Businesses that do not keep complete invoices and documents or have not filed tax reports for a long time often face difficulties when settling taxes during dissolution. Reviewing and completing accounting records is a necessary step before carrying out dissolution procedures.

For FDI enterprises, in addition to the business dissolution procedure, they must also carry out the procedure for terminating the investment project, handling the Investment Registration Certificate, and fulfilling obligations related to the foreign investor.

Many businesses have ceased operations or downsized, leaving them without accounting, legal, or administrative departments to handle the procedures. In such cases, using a business dissolution service helps ensure that the documentation is prepared correctly and minimizes the risk of errors.

Note: The longer a business has outstanding taxes, accounting or debt, the more complicated the dissolution process will be and the more time it will take to process.

Viet An Law Firm provides comprehensive business dissolution and company dissolution services for both domestic and foreign-invested enterprises (FDI). Depending on the specific case, we support you from the document review stage and tax obligation handling to completing the dissolution procedures at the competent state agency.

| Scope of Work | Scope of support |

| Legal advisory | Advise on conditions, orders, procedures, and appropriate dissolution plans. |

| Dossier drafting | Prepare the enterprise dissolution application dossier in accordance with current regulations. |

| Tax support | Review tax obligations, support tax finalization, and close the tax code. |

| Customs support | Work with the customs authority for enterprises engaged in import and export activities. |

| FDI enterprises | Support the termination of investment projects and relevant procedures concerning foreign investors. |

| Procedural representation | Work with state authorities on behalf of the enterprise under authorization. |

Viet An Law Firm assesses the legal status, tax obligations, debts, and other arising issues of the business to advise on a suitable dissolution plan. For cases where the tax code is locked, operations have ceased, or there are outstanding accounting records, we provide a processing roadmap before proceeding with dissolution.

We assist in preparing all necessary dissolution documents according to regulations, including the dissolution decision, dissolution notice, meeting minutes, asset liquidation documents, and other related documents.

This is the most time-consuming part of the company dissolution process. Viet An Law Firm assists in reviewing tax records, working with tax authorities, performing tax settlements, and completing procedures for terminating the tax code as required.

For businesses involved in import and export activities, we assist in working with customs authorities to confirm the completion of obligations before submitting the business dissolution application.

In addition to the business dissolution procedure, FDI enterprises must also carry out the procedure for terminating the investment project and handling issues related to the Investment Registration Certificate. Viet An Law Firm supports the entire process in accordance with investment law regulations.

According to the authorization, Viet An Law Firm can represent clients in submitting applications, receiving results, and working with the business registration authority, tax authority, customs authority, and other competent authorities during the business dissolution process.

Viet An Law’s company dissolution service is carried out professionally, assisting enterprises in handling all legal documents, settling taxes, and completing the company dissolution procedures in accordance with the law. Depending on whether the company dissolution is voluntary or mandatory, Viet An Law will advise on the most suitable option to optimize time and costs for the enterprise.

Viet An Law receives information, legal documents, and the actual operational status of the enterprise to assess its feasibility of carrying out the legal entity termination procedure.

The support services include:

Key contents of the dissolution decision include:

During the business closure procedures, the enterprise must liquidate assets and fully settle all debts in the order of priority stipulated in the Law on Enterprises 2020.

Asset liquidation may be carried out by:

carry out the liquidation process directly if the company’s charter does not stipulate a separate liquidation organization.

The company’s debts are paid in the following order:

Viet An Law assists enterprises in handling tax settlement for dissolution, closing the company’s tax code, and reviewing financial obligations before submitting company dissolution documents.

| Dissolution form | Execution process |

| Voluntary company dissolution | Approve the dissolution decision → Liquidate corporate assets → Notify the dissolution → Settle outstanding debts → Submit the dossier for termination of business operations. |

| Compulsory company dissolution | State authority notifies the dissolution status → The enterprise holds a meeting regarding the dissolution → Settle financial obligations → Submit the official company dissolution dossier |

Viet An Law represents clients in working with tax authorities, business registration agencies, customs, and other relevant agencies to support the processing of procedures quickly and in accordance with the law.

After completing the company closure documents, Viet An Law continues to monitor the processing status and support the enterprise until the dissolution status is updated on the national business registration system.

In the first five months of 2026, Viet An Law Firm assisted numerous domestic and foreign-invested enterprises in carrying out business dissolution procedures in Hanoi, Ho Chi Minh City, and many other provinces and cities nationwide.

Viet An Law Firm’s clients operate in various fields such as commerce, manufacturing, technology, education, restaurants, cosmetics, pharmaceuticals, import-export, and foreign investment. The support process included advising on dissolution plans, handling tax obligations, terminating tax identification numbers, completing legal documents, and carrying out procedures at competent state agencies.

With practical experience in handling business dissolution documents, foreign invested company dissolution, tax finalization and tax code termination, Viet An Law supports businesses in completing procedures in accordance with legal regulations, limiting risks and saving implementation time.

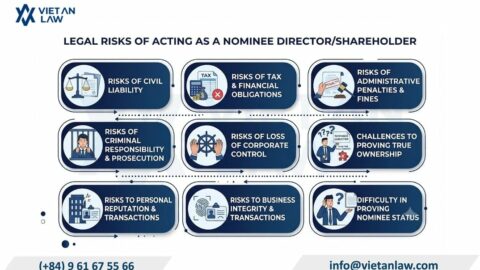

| Legal risks | Details |

| Rejection of company dissolution dossier | The enterprise does not clearly understand the legal process or prepares an incomplete dissolution dossier contrary to statutory regulations |

| Prolonged company closure timeline | Errors in tax procedures, asset liquidation, or debt settlement cause the company dissolution timeline to be significantly extended |

| Tax penalties and fines | Errors or mistakes during tax finalization for dissolution or close tax code in Vietnam can lead to administrative penalties. |

| Arising labor disputes | Failure to fully pay salaries, social insurance contributions, or severance allowances to employees |

| Ineligibility for company dissolution | The enterprise has not yet fulfilled its financial obligations, outstanding liabilities, or is still involved in ongoing court disputes. |

| Specific risks for foreign invested company dissolution | Failure to complete customs finalization procedures, terminate the investment project, or settle obligations with management authorities |

| Arising unexpected expenses | Dossiers requiring multiple re-submissions or undergoing intensive tax audits increase the total cost of terminating the legal person status |

| Joint and several liability of the legal representative | The representative may still bear personal liability for unfulfilled debts or outstanding financial obligations after the company closes |

In fact, to mitigate legal risks and save time processing paperwork, many enterprises choose to use company liquidation services to assist with tax settlement, closing the business’s tax code, and shutting down the company in accordance with the law.

When using company liquidation services or consulting company closure services at Viet An Law, clients need to provide certain necessary documents and records to support the process to close the company, settle taxes, and close tax code in Vietnam in accordance with legal regulations.

| Dossier | Specific documents |

| Enterprise Registration Certificate | A copy or the original copy of the ERC |

| Investment Registration Certificate | Applicable to FDI enterprises or foreign-invested companies |

| Corporate tax dossier | Notice of tax finalization, or confirmation of corporate tax identification number deactivation (if any) |

| Foreign investment report | Investment status report for FDI enterprises |

| Information on liabilities and financial obligations | Including loans, outstanding debts, and unfulfilled obligations to partners and employees |

| Accounting books and documents | Invoices, accounting vouchers, financial statements, and other relevant documents |

| Social Insurance dossier | Confirmation of completion of social insurance obligations or other labor-related duties |

| Other legal documents | Official dispatch confirming no outstanding tax debts, no outstanding social insurance contributions, or other relevant papers depending on specific cases |

Based on the client’s provided documents, Viet An Law will assist in consulting, reviewing the legal status of the business, preparing company dissolution documents, tax finalization for company dissolution, and completing the business closure procedures in accordance with current legal regulations.

| Task | Estimated time |

| Receipt of dossier | 1-2 days |

| Review of dossier | 3-5 days |

| Execution of procedures | Depending on the enterprise’s status |

| Completion of services | Subject to the results from state authorities |

Note: The times mentioned above are service times, not legal times.

The company dissolution costs in Vietnam are not fixed and will depend on the legal status, financial obligations, and actual documentation of each enterprise. During the business dissolution procedures, the following factors can directly affect the total cost of company dissolution:

| Influencing factors | Details |

| Corporate tax status | Enterprises that have not completed tax finalization, have outstanding tax debts, or have errors in tax declarations usually incur higher handling costs |

| Accounting books and records | Incomplete, unfinalized accounting dossiers or a large volume of arising invoices requiring review will increase the total cost of closing the company |

| Financial obligations and liabilities | Enterprises with outstanding loans, liabilities to partners, or unfulfilled obligations to employees will require additional processing time |

| Type of business entity | Dissolving an LLC, a Joint stock company, or an FDI enterprise involves different levels of complexity. |

| Import-export operational status | It is required to execute additional customs obligation verification procedures before deactivating the corporate tax identification number |

| Actual operational status | Enterprises that have been inactive for many years or have had their tax identification numbers locked typically incur additional handling procedures |

| Scope of dissolution services | Opting for a full-package dissolution service will include comprehensive legal consultation, tax dossier handling, and acting as the authorized representative to work with state authorities |

| Dossier processing time | Dossiers requiring urgent handling or triggering intensive tax audits can increase the overall execution costs |

In reality, the cost of dissolving a company is usually lower for enterprises with clear tax records, few outstanding debts, and full fulfillment of financial obligations. Conversely, enterprises with accounting errors, tax debts, or complex legal documentation will typically take more time and cost more to process when closing down.

As mentioned above, according to Article 207 of the Law on Enterprises 2020, for an enterprise to be eligible for dissolution, it must ensure that all debts and other financial obligations, including tax obligations and social insurance obligations to the State, are fully paid.

Therefore, if the company still owes taxes or social insurance contributions, its dissolution will not be approved according to regulations. In cases where the company is no longer able to pay and the business owner does not wish to continue operating, they can file a petition for bankruptcy proceedings with the competent court.

According to Clause 1, Article 213 of the Law on Enterprises 2020 (amended and supplemented in 2025), branches, representative offices, and business locations of enterprises may cease operations by decision of the enterprise itself or by decision of a competent state agency revoking the ERC, branch operation, representative office operation, or business location.

Although not directly stipulated, it can be understood that the branch or representative office of an enterprise will cease operations before the enterprise is officially dissolved (when the enterprise’s status is updated to “dissolved” on the National Portal for Enterprise Registration). Otherwise, after the company is dissolved, it will not have the authority to issue a decision to terminate the operations of its branch or representative office.

Currently, the law does not restrict business owners from establishing a new company immediately after dissolution. Therefore, business owners have the full right to establish a new company immediately after dissolving the old one, as long as the dissolution process has been carried out in accordance with the law.

Enterprises should use a company closure service when they encounter difficulties in handling tax matters, debts, labor obligations, or lack a dedicated department to handle legal procedures.

The service typically includes advising on dissolution conditions, reviewing the business’s legal status, preparing documents, settling taxes, closing the tax identification number, and representing the business in dealings with government agencies.

Yes. The consulting firm will assist in reviewing the cause, handling tax-related issues, and carrying out the necessary procedures before completing the dissolution process.

Yes. Businesses can authorize a law firm or legal consulting firm to represent them and perform tasks within the scope of their authorization.

Yes. This is a crucial aspect of the service, especially for businesses with outstanding issues regarding tax declarations, settlements, or tax obligations.

Yes. For businesses that have ceased operations for a long period, the consulting firm will assess their legal status and propose appropriate solutions.

Yes. The service applies to both domestic and foreign-invested enterprises, including procedures related to investment projects when necessary.

It depends on the case. When properly authorized, the service provider can act on behalf of the client to handle many tasks with competent authorities.

The service helps businesses save time, minimize errors in paperwork, reduce legal risks, and facilitate the handling of related procedures.

Viet An Law supports clients in Hanoi, Ho Chi Minh City, and many other provinces and cities nationwide for both domestic and FDI businesses.

Contact Viet An Law for advice and support in company dissolution to save time and optimize costs.