Learn the crucial steps to take when you’ve written a VAT invoice incorrectly, ensuring compliance and avoiding potential penalties while maintaining smooth business operations. VAT is a tax calculated on the added value of goods and services arising in the process from production, circulation to consumption. The VAT Law has come to life and has had a positive impact on a number of aspects such as encouraging investment and export, in line with international practices and facilitating economic integration for Vietnamese enterprises; reform administrative procedures and ensure revenue sources for the state budget. In the context that the tax industry is strengthening the supervision of e-invoices and combating tax fraud, accountants need to pay attention to carefully verifying the transparency of invoices to protect businesses from violations and avoid causing tax losses. However, in fact, there are many difficulties and errors that may occur in the process of issuing invoices, especially e-invoices. Viet An Tax Agent will provide information to businesses, organizations and individuals on how to handle erroneous invoices according to Circular 78 in the easiest and fastest way.

Principles for handling erroneous invoices according to Circular 78 and Decree 123

Pursuant to Clause 1, Article 7 of Circular 78/2021/TT-BTC, there are regulations on a number of new points on the content of handling erroneous e-invoices as follows

For e-invoices

In case the e-invoice that has been made has errors and must be re-issued with the tax authority’s code or the e-invoice has errors that need to be handled in the form of adjustment/replacement, the seller shall use the form No. 04/SS-HDDT to notify the adjustment of each invoice or many e-invoices with errors and send a notice to the tax authority (at the latest on the last day of the VAT declaration period for which the adjusted e-invoice is generated)

In case the seller makes an invoice to collect money first or collect money while providing services, but then the cancellation or termination of the service provision arises, the seller shall cancel the e-invoice and notify the tax authority of the cancellation of the invoice according to form No. 04/SS-HDDĐ

In case the e-invoice that has been made has errors and the seller has handled it in the form of adjustment/replacement, then detects that the invoice continues to have errors, in the next processing, the seller will perform in the form applied when handling the error for the first time

In case the e-invoice is made without an error in the invoice number, invoice symbol or invoice number, the seller shall only make adjustments without canceling or replacing them

In case there is an error in the value on the e-invoice, the adjustment shall be increased (written positively), adjusted down (marked negative) in accordance with the actual adjustment

In case of additional declaration of tax declaration dossiers related to adjusted or replaced e-invoices (including canceled e-invoices), the provisions of tax administration law shall apply.

For e-invoice data summary table

Pursuant to the provisions of Clause 2, Article 7 of Circular No. 78/2021/TT-BTC

In case the summary table sent to the tax authority lacks e-invoice data, the seller shall send an additional e-invoice summary table

In case the e-invoice data summary table sent to the tax authority has errors, the seller shall send adjustment information for the information declared on the summary table

Guidance on handling erroneous invoices according to Circular 78 and Decree 123

Case 1: The seller detects that the e-invoice has been issued a code by the Tax Authority but has not been sent to the buyer is made incorrectly

Legal basis: Clause 1, Article 19 of Decree 123/2020/ND-CP

Handling plan: Cancel the made invoice and issue a new invoice instead.

Processing process:

Case 2: Handling errors in invoices made or sent to buyers where the buyer or seller detects errors in the buyer’s name and address but the tax identification number is not wrong and other contents are not wrong.

Grounds: Point a, Clause 2, Article 19 of Decree 123/2020/ND-CP

Handling plan: Notify the invoice with errors to the buyer and the Tax Authority, do not have to re-make the invoice

Processing Process

Step 1: The seller sends a notice to the buyer about the error on the invoice and does not make a new invoice.

Step 2: The seller shall notify the tax authority of the incorrectly written or erroneous e-invoice according to Form 04/SS-HDDT

Case 3: Handling errors in invoices with incorrect tax codes, amounts written on invoices, tax rates, tax amounts or goods written on invoices in contravention of regulations and quality,…

Pursuant to Point b, Clause 2, Article 19 of Decree 123/2020/ND-CP, the seller and the buyer shall agree with each other to choose 1 of 2 settlement options as follows:

Option 1: Invoice adjustments for e-invoices with errors. The seller makes an e-invoice to adjust the invoice made with errors to send to the buyer

The e-invoice that adjusts the e-invoice that has been made with errors must have the words “Adjustment to the invoice Form No… ampersand… number… day… month… year”.

Contents to be written on the adjustment invoice: For an increase adjustment, a positive mark is marked, for a decrease adjustment, a negative mark is recorded in accordance with the actual adjustment

The seller digitally signs on the newly adjusted e-invoice for the erroneous e-invoice, then sends it to the buyer (For e-invoices without code) or sends it to the Tax Authority for issuing a code and then sends it to the buyer (For e-invoices with code).

In case the seller and the seller have an agreement on the making of an agreement before making and correcting errors, the two parties shall clearly state the errors in the written agreement.

Option 2: Alternative invoicing. The seller makes a new e-invoice to replace the erroneous e-invoice to send to the buyer

In case the seller and the buyer have an agreement on making a written agreement before making an invoice to replace the original invoice with errors, the 2 parties shall clearly state the error in the document, then the seller shall make an e-invoice to replace the invoice that has been made with errors.

The new e-invoice replaces the e-invoice that has been made with errors, must have the line “Replace the invoice Model No… ampersand… number… day… month… year”.

The seller digitally signs on the new e-invoice to replace the erroneous e-invoice and then sends it to the buyer (For e-invoices without code) or sends it to the Tax Authority to issue a code and then sends it to the buyer (For e-invoices with code)

Case 4: Cancellation or termination of service provision arises

Pursuant to Point b, Clause 1, Article 7 of Circular 78/2021/TT-BTC

Handling plan: Cancel the invoice

Implementation process

The seller cancels the e-invoice that has been made

Notification to the Tax Authority according to Form 04/SS-HDDT of the cancellation of invoices

Case 5: Handling erroneous paper invoices after switching to e-invoices.

Pursuant to Clause 6, Article 12 of Circular 78/2021/TT-BTC

Handling plan: Replace new e-invoicing

Processing process:

Case 6: The Tax Authority detects an invoice with an error and notifies the seller

Pursuant to Clause 3, Article 19 of Decree 123/2020/ND-CP

Processing process:

Step 1: Receive a notice of review from the Tax Authority

Step 2: Make an erroneous e-invoice notification to the Tax Authority

Step 3: Cancel/ Replace/ Adjust invoices, wait for the Tax Authority to issue a code and send it to the buyer

Case 7: Detecting that the Adjustment or Replacement invoice continues to have errors

Pursuant to Point c, Clause 1, Article 7 of Circular 78/2021/TT-BTC

Implementation process: In subsequent treatments, the seller follows the form applied when handling errors for the first time

Case 8: The e-invoice summary table sent to the tax authority has errors

Pursuant to Clause 2, Article 7 of Circular 78/2021/TT-BTC

Processing Process

In case of missing e-invoice data in the e-invoice data summary table, the seller shall send an additional e-invoice data summary table

In case the submitted data summary table has errors, the seller shall send adjustment information for the information declared on the summary table

The adjustment of invoices on the e-invoice data summary table must be filled in with full information: Symbol of the invoice number, invoice number in column 14 “Related invoice information” in Form 01/TH-HDDT.

If you have any difficulties or questions related to handling when writing the wrong VAT invoice, please contact Viet An Tax Agent for the most specific advice.

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

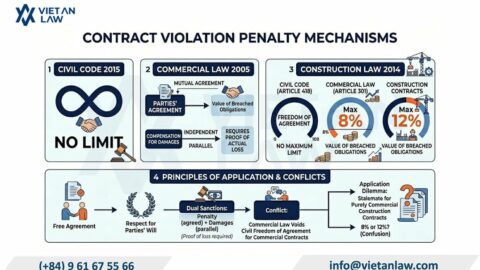

Vietnam's draft Commercial Law 2026 removes the 8% contract penalty cap, allowing unlimited breach penalties. Learn how this affects your contracts, liquidated damages clauses, and dispute strategy.

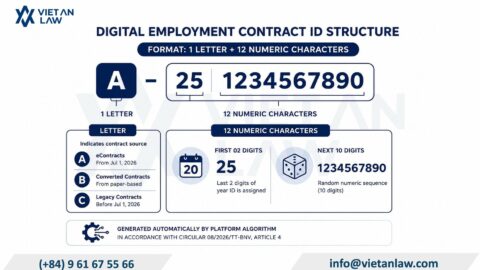

Electronic employment contract Vietnam: Complete guide to Circular 08/2026/TT-BNV key updates on ID codes, eContract platform access, and digital labor contract requirements effective July 2026.

Can you dissolve a company with a locked tax code in Vietnam? No—but dissolution is possible after restoring tax compliance. Learn the legal requirements, costs, timeline, and step-by-step procedures to…

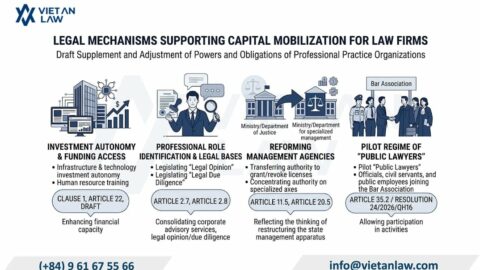

Capital contributing members in law firms Vietnam: Draft Law on Lawyers 2026 allows non-lawyer investors in limited liability law firms for the first time. Effective March 2027.

Avoid costly employment contract mistakes in 2026. Expert guide covers Labor Code 2019 compliance, contract types, social insurance, and common violations. Professional labor law consultancy from Viet An Law.