Instructions for updating and changing personal tax identification number information

The management and updating of personal tax identification number information is an important part of tax management, ensuring the rights and obligations of taxpayers. On June 20, 2024, the Ministry of Finance issued Circular 86/2024/TT-BTC, detailing the process, dossiers and forms of updating personal tax identification number information in the tax administration system. This Circular takes effect from August 1, 2024 and replaces a number of contents of previous documents to synchronize tax data and improve management efficiency. Viet An Tax Agent will provide specific instructions on how to update and change personal tax identification number information in accordance with the latest regulations, helping people and businesses to do it easily, quickly and accurately.

Table of contents

Hide

Legal documents according to Circular 86/2024/TT-BTC

According to Point b, Clause 1 and Clause 5, Article 5 of Circular 86/2024/TT-BTC, the Ministry of Finance has introduced new regulations on the structure of tax identification numbers, divided into two main groups, and at the same time there are important changes related to the use of personal identification numbers instead of tax identification numbers for some subjects. Concrete:

Tax identification numbers are divided into two main categories:

Tax identification numbers for enterprises and organizations: Directly issued by tax authorities in accordance with the provisions of Clauses 2, 3 and 4 of Article 5 of this Circular.

Tax identification numbers for households, business households and individuals: Including cases of being granted tax identification numbers as prescribed at Points a, dd, e, h, Clause 4, Article 5. In some cases, a tax identification number is no longer a series of numbers issued separately by the tax authority, but a personal identification number issued by the Ministry of Public Security, according to the provisions of Clause 5 of the same Article.

Personal identification numbers are used in place of tax identification numbers in the following cases:

Thus, according to the new regulations in Circular 86/2024/TT-BTC:

The tax identification numbers of individuals, dependents, households and business households will be consolidated and unified by personal identification numbers.

The use of personal identification numbers simplifies procedures, facilitates the process of tax management and lookup, and ensures synchronization with the national database on population.

What is the personal identification number of a Vietnamese citizen

The Law on Identity in 2023 has clearly and in detail stipulated the personal identification number – a unique code, playing a central role in determining the identity of each Vietnamese citizen in modern administrative management systems. According to Article 12 of this Law, the specific contents are as follows:

Personal identification numbers are:

It is a natural sequence of 12 digits, issued uniquely to each Vietnamese citizen.

Established by the National Population Database, ensuring that there is no duplication and no change throughout the life of each individual.

Competent agencies to establish and manage:

The Ministry of Public Security is the unified agency for managing personal identification numbers nationwide.

The issuance and management are carried out synchronously and integrated in the population database system to ensure efficiency and legality throughout the use process.

Purpose of using personal identification numbers:

Used for issuing citizen identification cards.

It is the key to looking up personal information in the National Population Database and other national databases, as well as specialized databases.

It is a unique identification code that helps citizens access and use online public services through the national public service portal, national data center, and other information systems for administrative procedures.

Places to submit dossiers of change of tax registration information for organizations

In case of changing tax registration information but not changing the tax authority directly managing it

In case the taxpayer changes the tax registration information but still belongs to the same tax authority directly managing it, the regulations are as follows:

In case of tax registration together with registration of enterprises, cooperatives and businesses:

When there is a change in tax registration information (e.g. name, industry, phone number, email, etc.), the taxpayer shall change the information at the same time as the change in the registration content of the enterprise, cooperative or business at the corresponding business registration office.

In case the taxpayer falls into the following subjects:

According to the provisions of Points a, b, c, d, dd, e, h, n, Clause 2, Article 4 of Circular 86/2024/TT-BTC (including organizations not subject to business registration, political organizations, social organizations, non-business units, non-governmental organizations, religious establishments, etc.), then:

Submit a dossier of change of tax registration information at the current directly managing tax authority.

Special cases:

For contractors and investors participating in petroleum contracts (specified at Point h, Clause 2, Article 4), when there is an event of transfer of contributed capital or transfer of petroleum contract interests, then:

File at the Tax Department where the operator is headquartered, or

At the Tax Department of Large Enterprises, if the executive is under the management of this agency.

In case of change of tax registration information changes the tax authority directly managing

When changing information leads to a change in administrative boundaries or the location of the head office, leading to the transfer of the tax authority for management, the implementation regulations are divided as follows:

In case of tax registration together with registration of enterprises, cooperatives and businesses:

If an organization moves its head office address to another province/centrally run city, or changes its address to another district/district in the same province/city, resulting in a change of directly managing tax authority, then:

Before submitting a dossier of change of address at the business registration agency, the organization needs to submit a dossier of change of tax registration information at the tax authority where the company moves to fully fulfill its tax obligations and necessary procedures.

In case the taxpayer is subject to direct tax registration with the tax authority (according to Points a, b, c, d, dd, h, n, Clause 2, Article 4 of Circular 86):

When there is a similar change in the address of the head office that changes the managing tax authority, two steps should be taken:

At the tax authority where the person is moving:

Submit a dossier to change tax registration information to complete obligations at the old place.

The tax authority will issue a Notice of relocation according to Form No. 09-MST (issued together with Circular 86/2024/TT-BTC).

At the tax authority where you move to:

Within 10 working days from the date of receipt of the notice from the tax authority of the place of relocation, the taxpayer must submit a dossier of change of tax registration information at the tax authority of the place of relocation to update the information in the system.

How to change tax identification number to personal identification number from 01/7/2025

In case the taxpayer does not have a tax identification number, the taxpayer registers the tax identification number for the first time through:

Directly at the local tax department; or

Online on the National Public Service Portal.

In case there is a tax identification number and the information has been correctly matched with the National Population Database

Applicable to business households, households and individuals who are granted tax identification numbers before July 1, 2025.

When the tax registration information has matched the information in the National Population Database:

Personal identification numbers will be used instead of tax identification numbers from July 1, 2025.

The adjustment and supplementation of tax obligations shall still comply with the previously issued tax identification numbers.

The tax authority keeps track of all tax data and family circumstance deduction information through personal identification numbers.

In case there is a tax identification number but the information does not match or is incomplete, when the tax registration information does not match or the data is missing compared to the National Population Database:

The tax identification number will be switched to the status of “waiting for personal identification number information to be updated” (status 10).

Taxpayers need to carry out procedures for updating and adjusting tax registration information with tax authorities according to Article 25 of Circular 86.

After the correct update, the personal identification number may be used instead of the tax identification number as prescribed in Article 38 of this Circular.

In case an individual has more than one tax identification number

Taxpayers must:

Update personal identification number information for all issued tax identification numbers.

The tax authority will consolidate tax identification numbers into a single personal identification number.

Invoices, vouchers and tax dossiers made in the past:

It is still legally valid for use in tax administrative procedures.

There is no need to modify the personal identification number.

If you have any difficulties or questions related to the service of updating and changing tax code information, please contact Viet An Tax Agent for the most specific advice.

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

Change Business Registration in Saigon Ward, HCMC guide. Complete procedures, required documents, timelines, and online submission process for enterprises in 2025.

Enterprise Registration Change in Xuan Hoa Ward, HCMC guide for 2026. Learn mandatory procedures, 10-day deadlines, online filing requirements, and avoid penalties up to 30M VND.

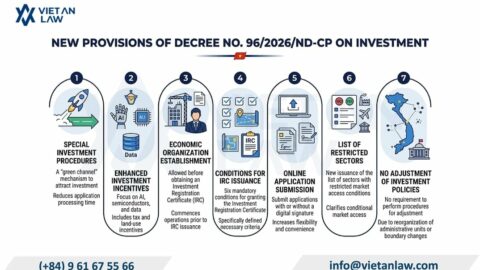

Decree 96/2026/ND-CP Guiding the Vietnam Investment Law 2025 introduces special investment procedures, new incentives for AI and semiconductors, and streamlined processes effective March 31, 2026.

Latest Updates on Tax Administration for Associated Transactions in Vietnam 2026. Complete guide covering transfer pricing, CbCR requirements, and compliance obligations.