How to declare PIT from the transfer of contributed capital & shares in Vietnam

The transfer of contributed capital and equity interests in Vietnamese enterprises triggers personal income tax obligations that require strict compliance with statutory declaration procedures under Vietnamese tax legislation. Taxpayers engaging in capital transfer transactions must fulfill specific reporting requirements within prescribed timeframes to ensure adherence to the Law on Personal Income Tax and its implementing regulations. The declaration process encompasses both the calculation of taxable income derived from capital gains and the submission of requisite documentation to competent tax authorities. In the article below, Viet An tax agent will guide you on how to declare PIT from the transfer of contributed capital and shares. Deadline for submitting PIT returns from the transfer of contributed capital and issues to note.

Table of contents

Hide

Instructions on how to declare PIT from the transfer of contributed capital in Vietnam

Principles when declaring PIT

Subjects being resident individuals: Resident individuals who transfer contributed capital must declare PIT for each transfer (regardless of whether or not taxable income is generated).

Non-resident individuals: Non-resident individuals who transfer contributed capital in the territory of Vietnam do not need to declare tax directly to the managing tax authority and the transferee will fulfill the obligation to declare. In case the transferee is an individual, it will declare personal income tax for each time it is incurred.

When transferring capital contribution, there are no grounds to determine that tax obligations have been fulfilled: If an enterprise or organization carries out procedures for changing the name of a capital contributor in case of transferring capital contribution in a joint-stock company but does not have documents proving that the individual making the transfer has fulfilled the tax obligation as prescribed, the organization, such enterprise must be responsible for declaring and paying tax on behalf of such individual.

What does the PIT declaration dossier from the transfer of contributed capital include?

A PIT declaration dossier from the transfer of contributed capital for each time income is generated includes:

PIT declaration from the transfer of contributed capital (Form No. 04/CNV – TNCN) issued according to TT80/2021/TT-BTC.

The Appendix to the detailed list of individuals transferring contributed capital (According to form No. 04-1/CNV – TN) applies to organizations that declare and pay taxes on behalf of many individuals.

Contract for transfer of contributed capital.

Payment documents proving the transfer of contributed capital.

The document determines the value of contributed capital on the accounting books.

Citizen identity card of the transferor.

A copy of the business registration certificate of the enterprise.

Submitting PIT declaration dossiers from the transfer of contributed capital

After preparing a complete set of PIT declaration dossiers from the transfer of contributed capital, it is necessary to submit it directly to the managing tax authority. The deadline for submitting dossiers and completing PIT obligations for each time incurred is no later than 10 days from the date the individual incurs tax obligations.

How to declare PIT from share transfer in Vietnam

Principles of PIT declaration

Individuals who transfer shares declare tax for each time they arise.

If an enterprise changes the list of shareholders in the company but cannot prove that the individual transferring shares has fulfilled the tax payment obligation, the enterprise should be responsible for declaring and paying tax on behalf of that individual.

PIT declaration dossier from share transfer

PIT return from securities transfer activities according to form No. 04/CNV-TNCN issued together with Circular 80/2021/TT-BTC.

A copy of the share transfer contract of the individual.

After preparing the tax declaration dossier, the individual needs to submit the tax return to the tax authority managing the enterprise – where the individual carries out the share transfer activity.

The deadline for performing the obligation to declare and pay PIT from transfer activities is before the enterprise changes the list of shareholders in the company.

Some questions related to how to declare PIT from the transfer of contributed capital & shares

When carrying out capital transfer activities, can an individual authorize the company to declare PIT?

Individuals who carry out the transfer of contributed capital and shares can directly submit the tax declaration to the managing tax authority or authorize the PIT declaration company on their behalf if they do not have a clear understanding of the dossier and procedures.

When making a declaration on behalf of the taxpayer, the organization needs to write the phrase “Declaration on behalf of the taxpayer” immediately before the phrase “Taxpayer or legal representative of the taxpayer”, sign and seal the company’s title.

Can PIT declaration dossiers from the transfer of contributed capital and shares be submitted online?

PIT declaration dossiers from the transfer of contributed capital and shares can be submitted directly on the https://canhan.gdt.gov.vn/ page.

Penalties for failing to submit PIT declaration dossiers from the transfer of contributed capital

Depending on the violation, a warning or a fine of from 2,000,000 VND to 25,000,000 VND may be imposed for those who fail to submit PIT declaration dossiers from the transfer of contributed capital and shares

Above is how to declare PIT from the transfer of contributed capital & shares that Viet An Tax Agent wants to share with the community. Hope our article will help you!

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

Vietnam LLC Formation guide: Complete post-incorporation procedures after obtaining your ERC. Learn required steps including board meetings, signage, bank accounts, and tax registration for compliance.

On March 12, 2026, the Ministry of Finance issued Circular 20/2026/TT-BTC: new guidance on Vietnam corporate income tax (CIT), implementing the Law on CIT 2025 and Decree 320/2025/NĐ-CP. Effective immediately…

According to Official Letter 2169/TPHCM-QLDN3 (March 2026) issued by the Ho Chi Minh City Tax Department, the regulations on tax incentives under Resolution 198/2025/QH15 and Decree 20/2026/ND-CP have been clarified:…

In the context of rapid digital transformation and the increasing demand for financial transparency, numerous new regulations on non-cash payments are continuously being introduced. These changes directly impact the financial…

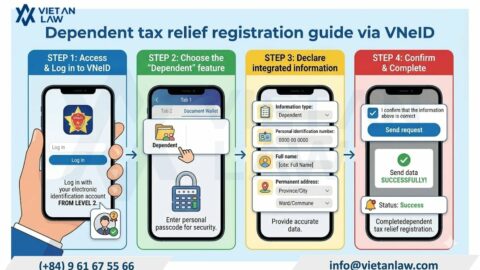

Learn how to register dependent deduction via VNeID in minutes. Step-by-step online guide covering documents, common errors, and 2026 PIT deduction rules. Start now!