Conditions for VAT Refund in Vietnam since July 2025

On July 1, 2025, the Value Added Tax Law 2024 (Law No. 48/2024/QH15) officially takes effect, marking an important adjustment step in Vietnam’s tax policy. Therein, regulations on VAT refunds are amended in a more specific and transparent direction, aiming to support enterprises but also to strengthen management and prevent fraud. So, what are the conditions to be eligible for a VAT refund after this point in time? The following article by Viet An Law will provide clients with specific conditions for enterprises to receive a value-added tax refund from July 1, 2025.

Some outstanding new points about VAT from July 1, 2025

The Law on Value Added Tax (VAT) 2024 was officially passed by the National Assembly at the 8th session, 15th National Assembly. This Law takes effect from July 1, 2025, replacing the Law on VAT No. 13/2008/QH12 which has been amended many times.

The VAT Law 2024 has outstanding new points that indirectly or directly affect tax refunds:

Reducing the VAT rate from 10% to 8% for goods and services currently subject to the 10% tax rate, applicable from July 1, 2025, to the end of December 31, 2026;

Adjusting the group of subjects not subject to VAT, increasing the non-taxable revenue threshold for individuals/business households from 100 million to 200 million VND/year;

Clarifying cases applying the 0% and 5% tax rates;

Amending the method of calculating the taxable price for imported goods;

Regulating non-cash payments (payment slips, electronic invoices, appropriate documents) to be eligible for input tax deduction in many specific cases;

Documents such as packing lists, bills of lading, and insurance documents (if any) are added as bases for deduction if they meet the requirements;

Abolishing tax refunds for ownership conversion, enterprise conversion, merger/consolidation, division/separation (except for dissolution and bankruptcy) if there is an un-deducted input VAT amount or overpaid tax amount.

Enterprises that import goods and subsequently export those goods to another country are not eligible for VAT refunds for exports, even if the export is carried out in customs operation areas.

Adding regulations on VAT refunds for expanded investment projects during the investment phase if the un-deducted input VAT amount of the investment project is 300 million VND or more.

Cases eligible for value-added tax refund

Based on Section 3, Chapter III of Decree 181/2025/ND-CP, cases eligible for VAT refund include:

Tax refund for exports

Tax refund for investment

Tax refund for goods and services subject to a 5% value-added tax rate

Tax refund for business establishments upon dissolution or bankruptcy

Tax refund for goods purchased in Vietnam and brought along upon departure

Tax refund for programs and projects using non-refundable ODA capital or non-refundable aid, humanitarian aid

Tax refund for goods and services purchased in Vietnam by subjects entitled to diplomatic privileges and immunities

Tax refund according to international treaties

Applicable to business establishments if the un-deducted input tax amount is 300 million VND or more after 12 consecutive months or 4 consecutive quarters.

Cases not eligible for value-added tax refund

Below are the cases not eligible for a value-added tax (VAT) refund according to current regulations:

When an enterprise makes changes in ownership or reorganizes (conversion, merger, consolidation, division, separation), the un-deducted VAT amount will not be refunded. Cases of dissolution or bankruptcy are handled differently, toward finalization to determine the final tax obligation.

2. Business activities of goods and services not subject to VAT

Enterprises doing business in goods and services that are not subject to VAT will not be eligible for tax refunds. Exception: Cases where exported goods and services are subject to a 0% tax rate are still eligible for tax refunds as prescribed.

Taxpayers who have not fully submitted VAT declaration dossiers according to the tax period or still owe VAT will not be considered for a tax refund. Only after completing the obligations of tax declaration and full tax payment will the refund be resolved.

4. Investment projects subject to tax transfer

For some investment projects in the implementation phase, the un-deducted input VAT amount will not be refunded immediately but must be carried forward to the next period for continued deduction.

This regulation applies to projects belonging to the list of non-refundable taxes according to the law (e.g., investment in resource and mineral exploitation; some specific sectors).

👉 Thus, not every un-deducted VAT amount is refunded. Enterprises need to carefully review their activities, projects, and tax declaration dossiers to determine whether they are eligible for a refund or must carry it forward to the next period.

Before July 1, 2025, the conditions to be eligible for a tax refund are:

Requiring enterprises to pay tax via the deduction method, having full accounting books

Having a bank account

Valid input invoices and documents;

The seller has declared and paid tax

No tax debts.

After July 1, 2025, it is similar to the above requirements but is made clearer. Specifically stipulated in Clause 9, Article 15 of the VAT Law 2024 and Article 37 of Decree 181/2025/ND-CP detailing the implementation of a number of articles of the VAT Law:

Conditions regarding subjects

Business establishments falling into the cases eligible for tax refund must be business establishments paying value-added tax under the tax deduction method;

Must prepare and preserve accounting books and accounting documents in accordance with the law on accounting;

Have a deposit account at a bank according to the tax code of the business establishment.

Meet the regulations on input value-added tax deduction and do not fall into the cases specified in Clause 15, Article 23 of Decree 181/2025/ND-CP;

Meet the regulations on input value-added tax deduction according to Clause 2, Article 14, and do not fall into the cases specified in Clause 3, Article 14 of the VAT Law 2024 (for the case in Clause 9).

Conditions regarding invoices and documents

The seller has declared and paid value-added tax in accordance with regulations for the invoices issued to the business establishment requesting the tax refund;

At the time of submitting the tax refund dossier, the seller has submitted the value-added tax declaration dossier as prescribed and no longer owes value-added tax for the corresponding tax period;

The tax management agency determines that the seller has declared and paid value-added tax based on the processing results of the automated information technology system;

In case the seller has not fully submitted the tax declaration dossier or still owes value-added tax, the business establishment will not be refunded tax for the corresponding invoices.

Conditions regarding the un-deducted input tax amount

Export: If the un-deducted input VAT amount is 300 million VND or more;

Investment projects: If a new/expanded investment project in the investment phase has an un-deducted input VAT amount of 300 million VND or more;

Business establishments only operating with goods and services subject to a 5% tax rate: After 12 consecutive months or 4 consecutive quarters, if the un-deducted input tax amount is 300 million VND or more.

Conditions regarding dossiers and procedures

At the time of submitting the tax refund dossier, the business establishment falls into the case of value-added tax refund, has an input tax amount meeting the conditions, and complies with the regulations on tax declaration under the law on tax administration.

Prepare a value-added tax refund dossier for each tax refund case and send it to the competent tax authority for receipt.

The tax authority classifies the tax refund dossier into the category of tax refund before inspection or inspection before tax refund and resolves the dossier according to the provisions of the law on tax administration.

Above are the conditions for VAT refund from July 01, 2025. The new regulations on VAT refunds create favorable conditions for enterprises subject to low tax rates but they still need to pay attention to the conditions to get a tax refund. If clients have further questions regarding the above VAT refund issues, please contact Viet An Law for our dedicated answers.

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

Learn how to reactivate locked tax code Vietnam in 6 fastest steps (2026). Complete guide covers causes, procedures, and common mistakes to restore your tax code quickly.

Inactive company Vietnam? Learn whether to suspend or dissolve your business. Expert guide on legal consequences, procedures, and optimal solutions for non-operating enterprises.

Vietnam abolishes copyright assessment certificate procedures from July 2026 under Decision 1198. Learn how this reform reduces compliance costs and impacts IP organizations.

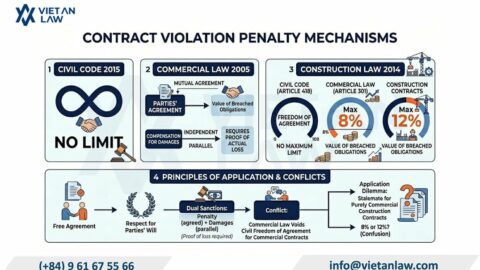

Vietnam's draft Commercial Law 2026 removes the 8% contract penalty cap, allowing unlimited breach penalties. Learn how this affects your contracts, liquidated damages clauses, and dispute strategy.

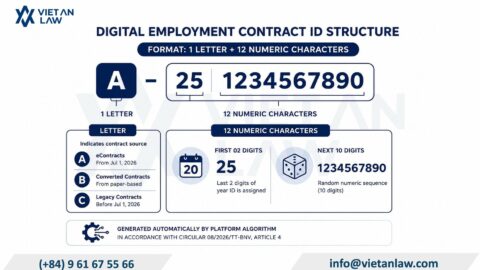

Electronic employment contract Vietnam: Complete guide to Circular 08/2026/TT-BNV key updates on ID codes, eContract platform access, and digital labor contract requirements effective July 2026.