Proposed Personal Income Tax Relief Levels in Vietnam for 2026

In the context of significant socio-economic fluctuations, with increasing changes in people’s income and cost of living, adjusting personal income tax policies has become necessary to ensure fairness and alignment with practical realities. Recently, the Ministry of Finance proposed adjusting the family circumstance reduction levels, to be applied from the 2026 tax period, aiming to better support taxpayers and alleviate the financial burden on households. In the article below, Viet An Law will provide clients with some information about the proposed personal income tax relief levels in Vietnam for 2026.

Who is currently subject to personal income tax (PIT)?

Pursuant to Article 2 of the Law on Personal Income Tax 2007, individuals subject to PIT include:

Residents who earn taxable incomes inside and outside the Vietnamese territory must meet the following conditions:

Being present in Vietnam for 183 days or more in a calendar year or 12 consecutive months, counting from the first date of their presence in Vietnam;

Having a place of habitual residence in Vietnam, which is a registered place of permanent residence or a rented house for dwelling in Vietnam under a term rent contract.

Non-residents who earn taxable incomes inside the Vietnamese territory.

What is the family circumstance reduction?

Pursuant to Clause 4, Article 1 of the Amended Law on Personal Income Tax 2012, reduction based on family circumstances means a sum of money deductible from pre-tax income from business, salary, or wage of a resident taxpayer. Thus, reduction based on family circumstances is only applicable to resident individuals with income from business activities, salaries, and wages. Reduction based on family circumstances consists of the following two parts:

Reduction for the taxpayer;

Reduction for each dependent of the taxpayer.

Proposed personal income tax relief levels in Vietnam for 2026

Currently, according to Resolution 954/2020/UBTVQH14, the reduction based on family circumstances levels on PIT being applied are as follows:

Reduction level for the taxpayers themselves is 11 million VND/month (132 million VND/year);

Reduction level for each dependent is 4.4 million VND/month.

In the draft Resolution on adjusting the reduction based on family circumstances levels on PIT levels submitted by the Ministry of Finance to the Ministry of Justice for appraisal, the Ministry of Finance proposes adjusting the FCD levels from 2026 as follows:

For the taxpayers themselves, raising the reduction level to 15.5 million VND/month (186 million VND/year);

For each dependent, raise the reduction level to 6.2 million VND/month.

The adjustment of the reduction based on family circumstances levels is necessary and consistent with price fluctuations, which are influenced by factors such as average per capita income, average GDP, and average per capita spending over a certain period. According to data from the General Statistics Office, the fluctuation in average per capita income and average per capita GDP has increased by approximately 40-42% since 2020. Therefore, raising the reduction based on family circumstances levels as proposed in the draft is deemed appropriate to the reality, contributing to reducing the tax burden on taxpayers amid rising prices and inflation.

When will the new family circumstance reduction levels be applied?

Pursuant to Article 2 of the draft Resolution on adjusting the reduction based on family circumstances levels on PIT levels, which stipulates the effective date, if the draft Resolution is passed, the new reduction based on family circumstances levels on PIT levels is expected to be applied from the 2026 tax period.

Definition of dependants and the basis for determination

Pursuant to Clause 3, Article 12 of Decree 65/2013/ND-CP, dependants whom the taxpayer has the obligation to support are defined as follows:

Children (including blood children, legally adopted children, stepchildren of spouse) who fall into the following cases:

Under 18 years old (calculated fully by month);

Disabled children who are aged 18 years or older and incapable of working;

Children who are studying at universities, colleges, professional secondary schools, or job-training schools and have no income or have an income of less than 1,000,000 VND/month.

Spouses of taxpayers; Blood parents or stepfather, stepmother, legally adopted parents, spouse’s parents of taxpayers; Other helpless individuals whom taxpayers are obliged to directly nurture are disabled, incapable of working, and have no income or have an income of less than 1,000,000 VND/month.

Principles for applying the reduction based on family circumstances for dependants

The reduction based on family circumstances for dependants is implemented based on the following principles:

The taxpayer may make reductions for his or her dependants if the taxpayer has applied for tax registration and been issued with the tax code;

When registering reductions for dependants, the taxpayer shall be issued with tax codes for dependants;

The period eligible for deduction starts from the date of registering reductions for dependants;

The deduction for a dependant shall apply to only one taxpayer in the tax year;

Where multiple taxpayers have the same dependent to provide for, they shall reach an agreement on the person who makes the deduction for such a dependent.

Determining the reduction based on family circumstances for the taxpayer themselves

The taxpayer who has multiple sources of income from wages and business shall calculate the personal reduction for himself in a place at a time (considered a full month);

The foreigner, being a resident in Vietnam, shall make a personal reduction from January (or the month of arrival if the person comes to Vietnam for the first time) until the month in which the labor contract expires, and that person leaves Vietnam in the tax year (considered a full month);

If the person has not made a personal reduction or the reduction does not cover 12 months in the tax year, the person may reduce for 12 months before settling tax.

The formula for calculating taxable income after the reduction based on family circumstances

To determine the taxable income used as the basis for calculating PIT, enterprises and individuals can apply the following formula:

Taxable Income=Total Income−(Taxpayer reduction based on family circumstances +Dependant reduction based on family circumstances)

Example: Ms. H has a total income of 25 million VND/month and one dependent. From 2026, Ms. H’s taxable income will be: 25 million VND−(15.5 million VND+6.2 million VND) = 3.3 million VND. According to the Partially Progressive Tax Schedule, the applicable tax rate for Ms. H’s taxable income is 5%. Thus, the PIT amount Ms. H must pay is 3.3 million VND×5% = 165,000 VND.

Procedures for the reduction based on family circumstances implementation

The reduction based on family circumstances for the taxpayer themselves will be directly subtracted when calculating taxable income.

For the reduction based on family circumstances for dependants, registration for dependant reduction based on family circumstances must be performed. Taxpayers with income from salaries and wages below 11 million VND/month (the currently applied level) are not required to declare dependants. Taxpayers with income from salaries and wages above 11 million VND/month shall register dependants as follows:

Step 1: The taxpayer submits 02 sets of the dependant registration dossier to the organization or individual paying the income, including:

The tax registration declaration form;

Dossiers proving the dependent status;

The deadline for submitting the dependant proof dossiers is within 03 months from the date of submitting the dependant registration declaration form.

Step 2: The organization or individual paying the income keeps 01 set and submits 01 registered set to the directly managing tax authority at the same time as submitting the PIT declaration for that tax period.

Above is the information on the issue of proposed personal income tax relief levels in Vietnam for 2026. Clients who have related questions or need legal support, please contact Viet An Law Firm – Tax Agent for the best support!

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

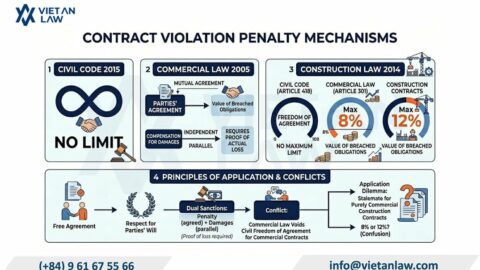

Vietnam's draft Commercial Law 2026 removes the 8% contract penalty cap, allowing unlimited breach penalties. Learn how this affects your contracts, liquidated damages clauses, and dispute strategy.

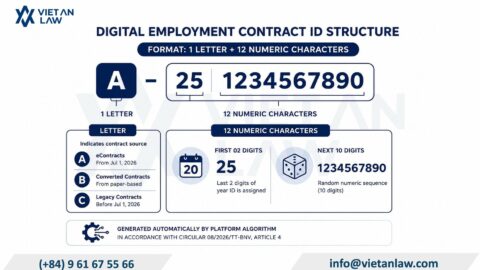

Electronic employment contract Vietnam: Complete guide to Circular 08/2026/TT-BNV key updates on ID codes, eContract platform access, and digital labor contract requirements effective July 2026.

Can you dissolve a company with a locked tax code in Vietnam? No—but dissolution is possible after restoring tax compliance. Learn the legal requirements, costs, timeline, and step-by-step procedures to…

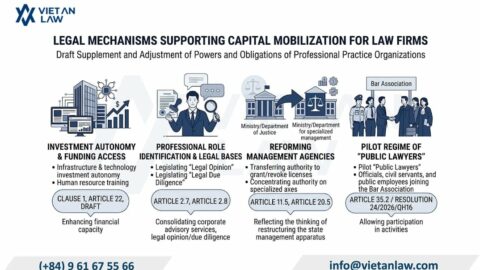

Capital contributing members in law firms Vietnam: Draft Law on Lawyers 2026 allows non-lawyer investors in limited liability law firms for the first time. Effective March 2027.

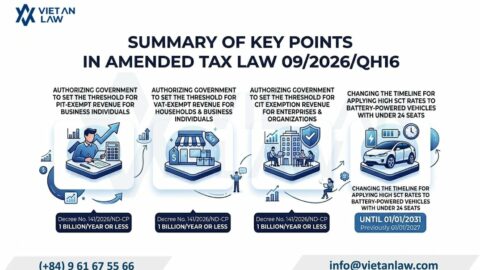

Law 09/2026/QH16 raises tax exemptions to 1 billion VND for household businesses. Learn PIT, VAT, CIT changes 2026 and who benefits most from Vietnam's new tax thresholds.