Capital Criteria for 3-Year Tax Exemption for Household Business Conversion in Vietnam

When converting from a household business to an enterprise, the newly established business will receive numerous incentives, such as those related to business registration, license fees, and corporate income tax. This aims to encourage household businesses to convert into enterprises to enhance professionalism and expand investment opportunities. So, what are the capital criteria for a 3-year tax exemption for household business conversion? In the article below, Viet An Law will advise and answer this question for our clients.

Capital criteria for 3-year tax exemption for household business conversion

On May 4, 2025, the Party Central Committee issued Resolution 68-NQ/TW of 2025 on the development of the private economy.

Specifically, based on Sub-section 2.1, Section 2, Part III of Resolution 68-NQ/TW of 2025 on accelerating reform and improving the quality of institutions and policies for small and medium-sized enterprises (SMEs), it states: Introduce special mechanisms and policies to assist small and medium-sized enterprises (SMEs) in accordance with market principles and international commitments; remove registration fees; exempt corporate income tax for SMEs during their first three years of operation.

Furthermore, according to Article 10 of Resolution 198/2025/QH15, passed by the National Assembly on May 17, 2025, on tax, fee, and charge support, it is stipulated: The corporate income tax for small and medium-sized enterprises shall be exempted for 3 years from the date of issuance of the first enterprise registration certificate.

Thus, according to the regulations above, the 3-year tax exemption policy for household business conversion applies to:

Subject: The policy only applies to conversions from a household business;

Business establishment: The established business must be a small or medium-sized enterprise;

Tax exemption: Corporate income tax;

Exemption period: 3 years from the date of issuance of the first enterprise registration certificate.

Overview of capital criteria for 3-year tax exemption for household business conversion

To be eligible for a 3-year tax exemption when converting from a household business to an enterprise, the converted business must be an SME.

Small and medium-sized enterprises include:

Micro-enterprises;

Small enterprises;

Medium-sized enterprises.

According to Article 4 of the Law Provision of Assistance for small and Medium-sized Enterprises 2017, the criteria for the identification of SMEs are as follows :

The annual average number of employees who participate in social insurance is not greater than 200;

Satisfying one of the following criteria:

The total capital is not greater than 100 billion dong;

The enterprise’s revenue of the previous year is not greater than 300 billion dong.

Micro-, small, and medium-sized enterprises are identified according to each industry, such as agriculture, forestry, aquaculture, industry and construction, and trade and services.

Capital criteria for 3-year tax exemption for household business conversion

Article 5 of Decree 80/2021/ND-CP provides specific criteria for identifying small and medium-sized enterprises. The capital criteria for a 3-year tax exemption for household business conversion are as follows:

Micro-enterprises

Micro-enterprises in the field of agriculture, forestry, aquaculture; industry, and construction: Total revenue in the year not exceeding 3 billion VND.

Micro-enterprise in the field of commerce and services: Total revenue in the year not exceeding 3 billion VND.

Example: Mr. A has a household business selling agricultural products in Dak R’lap district, Dak Nong province. In 2024, he decided to convert his household business into A Nong San Co., Ltd., with a total capital of 2.5 billion VND. Since the business is in the agricultural sector with a total capital of 2.5 billion VND (calculated based on the financial statement from the preceding year), Mr. A’s business is identified as a micro-enterprise.

Small enterprises

Small enterprise in the field of agriculture, forestry, aquaculture; industry, and construction: Total revenue in the year not exceeding 20 billion VND.

Small enterprise in the field of commerce and services: Total revenue in the year not exceeding 50 billion VND;

Example: Mr. C has a household business manufacturing furniture in Binh Duong. He converted it into Cuong Phat Wood Co., Ltd. with a total capital of 19.8 billion VND. Since the total capital does not exceed 20 billion VND and the company operates in the industrial sector, it is identified as a small enterprise.

Medium-sized enterprises

Medium enterprise in the field of agriculture, forestry, aquaculture; industry, and construction: Total revenue in the year not exceeding 100 billion VND;

Medium enterprises in the field of commerce and service: Total revenue in the year not exceeding 100 billion VND.

Example: Ms. B has a household business selling gold jewelry in Ho Chi Minh City. When she converted it into Bao Tin Gold Trading Co., Ltd., the company’s charter capital was 110 billion VND. With total capital exceeding 100 billion VND, Ms. B’s company does not meet the criteria to be identified as a medium-sized enterprise and is therefore ineligible for the 3-year corporate income tax exemption.

Guidance on how to determine the total capital of an SME

According to Article 8 of Decree 80/2021/ND-CP, the total capital of an SME is determined as follows:

The total capital of a year is determined in the balance sheet and specified on the financial statement of the preceding year, which is submitted by the enterprise to the tax authority. The total capital of a year shall be determined at the end of the year.

In case an enterprise has been operating for less than 01 year, the total capital shall be determined in the balance sheet of the enterprise at the end of the latest quarter before the enterprise applies for assistance.

SME declaration form

The declaration form for identifying an SME and proposing support is provided in the Appendix attached to Decree 80/2021/ND-CP.

Note:

Each SME shall complete the declaration form provided in the Appendix hereof, specify whether it is a micro-enterprise, small enterprise, or medium enterprise, and submit the form to the assisting authority. SMEs shall be responsible for their declaration.

In case an enterprise is found to have declared its scale incorrectly, it shall revise the declaration before assistance is provided.

In case an enterprise deliberately declares its scale incorrectly for the purpose of receiving assistance, it shall take legal responsibility and return the funds provided as assistance.

Other incentives for SMEs converting from household businesses

According to Section 1, Chapter IV of Decree 80/2021/ND-CP, SMEs converting from household businesses are also eligible for the following incentives:

Assistance in counseling, preparation of documentation and completion of procedures for enterprise establishment: The People’s Committees of provinces shall assign their Departments of Planning and Investment to provide counseling and instructions for household businesses to convert into enterprises free of charge regarding the following issues: Documentation and procedures for enterprise registration; Documentation and procedures for registration of the certificate of eligibility for conditional business lines (if any);…

Assistance in enterprise registration and publishing of the enterprise’s information: SMEs that are converted from household businesses will be exempted from paying the fee for enterprise registration for the first time at the business registration authority, and the fee for publishing the enterprise’s information for the first time on the National Enterprise Registration Portal.

Assistance in completion of procedures for registration of conditional business lines: An SME that is converted from a household business that keeps operating in their conditional business lines without changing the scale shall submit a request to the relevant competent authorities to be granted documents about fulfillment of business conditions.

Assistance in licensing fees: SMEs converted from household businesses will be exempted from licensing fees for 03 years from the issuance of the first Certificate of Enterprise Registration.

Counseling, instructing completion of tax procedures and accounting: SMEs converted from household businesses will receive complimentary counseling and instructions about completion of tax procedures and accounting for 03 years from the issuance of the first Certificate of Enterprise Registration.

Above is the information on the issue of capital criteria for a 3-year tax exemption for household business conversion. Clients who have related questions or need legal support, please contact Viet An Law Firm for the best support!

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

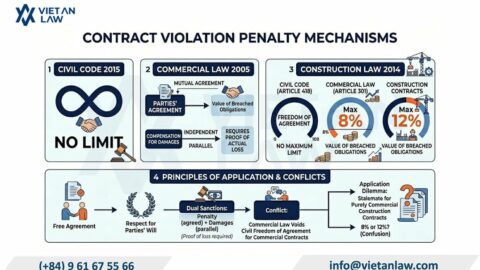

Vietnam's draft Commercial Law 2026 removes the 8% contract penalty cap, allowing unlimited breach penalties. Learn how this affects your contracts, liquidated damages clauses, and dispute strategy.

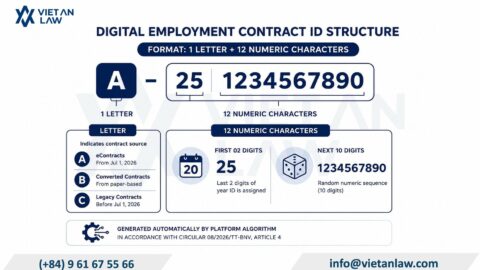

Electronic employment contract Vietnam: Complete guide to Circular 08/2026/TT-BNV key updates on ID codes, eContract platform access, and digital labor contract requirements effective July 2026.

Can you dissolve a company with a locked tax code in Vietnam? No—but dissolution is possible after restoring tax compliance. Learn the legal requirements, costs, timeline, and step-by-step procedures to…

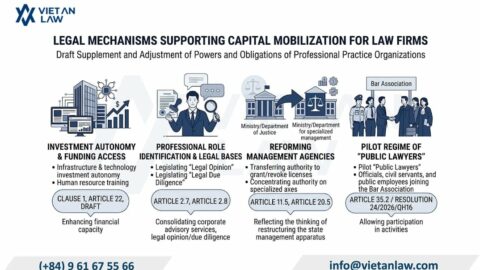

Capital contributing members in law firms Vietnam: Draft Law on Lawyers 2026 allows non-lawyer investors in limited liability law firms for the first time. Effective March 2027.

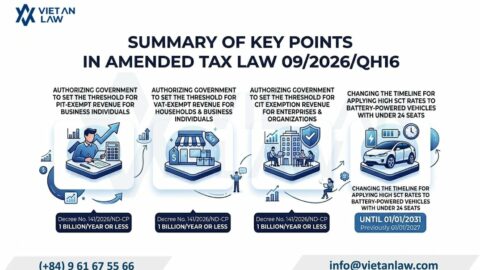

Law 09/2026/QH16 raises tax exemptions to 1 billion VND for household businesses. Learn PIT, VAT, CIT changes 2026 and who benefits most from Vietnam's new tax thresholds.