(Regulated under Decree 236/2025/ND‑CP guiding the implementation of Resolution 107/2023/QH15)

On November 29, 2023, the National Assembly adopted the resolution to apply global anti-tax evasion via a supplemental corporate income tax under global base erosion rules, effective from January 1, 2024. The global minimum tax is, in essence, a supplemental corporate income tax applied in cases where the effective tax rate is lower than the minimum rate proposed by the OECD for global application. The introduction of such a tax in Vietnam aligns with the Party and State policies. To provide details on Resolution 107/2023/QH15, on August 29, 2025, the Government issued Decree 236/2025/ND‑CP, specifying how global anti-tax evasion: new corporate income tax rules in Vietnam are to be applied. Below, Viet An Law Firm outlines the key points of this new regulation.

What Is the Corporate Income Tax Supplement under Global Base Erosion Rules?

On October 8, 2021, the OECD announced the Two‑Pillar Solution framework, under which the second pillar establishes a 15% global minimum tax for multinational enterprises to deter global anti-tax evasion via profit shifting to low-tax jurisdictions. For this mechanism, a multinational enterprise whose consolidated revenue reaches at least EUR 750 million in at least two of the four consecutive years preceding the year under review is subject to this global minimum tax. If its effective tax rate is below 15%, global anti-tax evasion requires a supplemental tax to cover the difference.

By December 16, 2022, the Inclusive Framework on BEPS (IF) announced that 138 jurisdictions had assented (no objection) to the Two‑Pillar framework, confirming global consensus behind measures to curb tax avoidance in the digital economy. Vietnam became the 100th member of BEPS and offered no reservations, thus becoming one of the endorsers. As of now, all 142/142 IF member jurisdictions have reached consensus on the Two‑Pillar framework — a foundation for global Anti‑Tax evasion.

In the context where major capital-exporting countries plan to adopt the global minimum tax to assert taxing rights, peer countries like Vietnam are studying response policies and investor support.

Clause 1 Article 3 of Resolution 107/2023/QH15 states: “Global Anti-Base Erosion (GloBE) rules are the rules provided for by this resolution and regulations of the Government in conformity with the global minimum tax regulations of the Inclusive Framework on Base Erosion and Profit Shifting (IF on BEPS) of which Vietnam is a member.”

This tax is termed supplemental because it does not replace the ordinary corporate income tax, but supplements only the shortfall if the locally effective rate is below 15%

Thus, the global anti-tax evasion is the tax imposed under the context of OECD and G20’s Two‑Pillar solution (BEPS 2.0), specifically Pillar 2, which sets a global minimum rate on corporate income.

Opportunities that the global anti-tax evasion: new corporate income tax rules bring to Vietnam

Applying the global minimum tax rules offers new prospects to Vietnam, namely:

Increasing state budget revenue via supplemental tax: Previously, many FDI groups benefited from low or exempted CIT (5–10%), causing revenue losses. Under minimum tax rules, Vietnam can claim the missing supplemental tax instead of allowing the parent country to collect it.

Enhancing international integration: Applying global anti-tax evasion helps Vietnam align its tax system with international practices by reforming CIT policies and relevant legislation.

Minimizing tax evasion, avoidance, transfer pricing, and profit shifting:

The fact that many countries have enacted corporate income tax incentives to attract foreign investment has made the practices of tax evasion, tax avoidance, transfer pricing, and profit shifting increasingly complex. Companies have exploited these opportunities to shift profits from high-tax jurisdictions to ones with lower tax rates, resulting in significant tax revenue losses.

Entities liable under global anti-tax evasion: new corporate income tax rules in Vietnam

Pursuant to Article 2 of Resolution 107/2023/QH15 and Article 3 of Decree 236/2025/ND‑CP, entities required to pay the supplemental CIT under global base erosion rules include:

Component entities of a multinational group whose consolidated revenue in the group’s ultimate parent company’s financials is at least EUR 750 million in 2 of the 4 preceding years, with exceptions including:

Governmental entities;

International organizations;

Nonprofit organizations;

Pension funds;

Investment funds as ultimate parent companies;

Real estate investment vehicles as ultimate parent companies;

Entities with at least 85% of their asset value owned (directly or indirectly) by the above types.

Some clarifications:

A “component entity” includes any company or organization in the group and any permanent establishment of such, including the ultimate parent, intermediate parents (if any), partially owned parent companies, and other business units or establishments within the group.

A multinational enterprise is defined as one having at least one component or establishment located outside the country of its ultimate parent.

The revenue threshold of 750 million EUR or more shall be determined according to the consolidated revenue of the Ultimate Parent Entity under the following specific circumstances: If one or more fiscal years of the MNE Group span a period other than 12 months, the revenue threshold of 750 million EUR for each of these fiscal years shall be determined based on the number of days in that fiscal year divided by 365. Determination of consolidated revenue of the Ultimate Parent Entity in case of merger or consolidation in any fiscal year of the four fiscal years preceding the fiscal year in which tax liability is being determined, in accordance with the guidance at point b, clause 2, Article 3 of Decree No. 236/2025/NĐ-CP

Standard domestic minimum supplemental tax formula under global anti-tax evasion: new corporate income tax rules in Vietnam

According to Article 4 of Resolution 107/2023/QH15 and Articles 4 and 5 of Decree 236/2025/ND‑CP, a constituent entity or a group of constituent entities of a multinational enterprise that is a taxpayer engaged in production or business in Vietnam, and whose residence in Vietnam is determined under Section I of Appendix II, must apply the rules on the Qualified Domestic Minimum Top-Up Tax (QDMTT)

If a multinational group has more than one constituent entity in Vietnam, the constituent entity responsible for filing returns is also responsible for determining the obligations under QDMTT for all constituent entities of that multinational group in Vietnam.

Accordingly, the amount of the Qualified Domestic Minimum Top-Up Tax(QDMTT) is determined by the following formula:

The Qualified Domestic Minimum Top-Up Tax for enterprises = (The Top-up Tax Rate x Excess profit) + Additional Current Top-up Tax (if any).

Where:

Top-up tax rate

The top-up tax rate is determined by: Top-up tax rate = Minimum tax rate – Effective tax rate. The top-up tax rate is rounded to the fourth decimal place.

The minimum tax rate is 15%.

Effective Tax Rate in Vietnam shall be calculated every fiscal year using this formula:

Effective Tax Rate in Vietnam

=

Regulated total corporate income tax accrued in Vietnam in the fiscal year of constituent entities

Covered corporate income tax in Vietnam include: Taxes recorded in the accounting books that relate to the incomes or profits of a Constituent Entity, or to the portion of incomes or profits of another Constituent Entity in which the entity holds an ownership interest; other taxes of a similar nature to corporate income tax, except: top-up tax pre-accrued by the Ultimate Parent Entity under a Qualified IIR (if applicable); top-up taxes pre-accrued by a Constituent Entity under QDMTT regulations; taxes on incomes from investment paid by a Constituent Entity that is an insurer on behalf of policyholders.

Adjusted covered corporate income tax in Vietnam is the amount of corporate income tax incurred in Vietnam that is covered by Point b.1 of this Clause and adjusted by Points 7 through 11, Section II of Appendix II of Decree 236/2025/ND-CP

Excess Profit

Excess Profit shall be determined by this formula:

Excess Profit = Net GloBE Income – Tangible asset carve-out and payroll carve-out (Substance-Based Income Exclusion) under the GloBE Rules.

Note:

Net GloBE Income shall be determined in accordance with Clause 7 Article 4 of Resolution No. 107/2023/QH15, ensuring that the income or loss of each Constituent Entity under the GloBE Rules are the net income or loss reported in the financial statements (prepared under the same financial accounting standards used for preparation of the consolidated financial statements of the Ultimate Parent Entity) of that Constituent Entity for the fiscal year in which the tax liability is being determined before any consolidated adjustment is made to eliminate intra-group transactions, and shall be adjusted in accordance with Points 1 through 5 Section II of Appendix II.

Tangible asset carve-out and payroll carve-out (Substance-Based Income Exclusion) under the GloBE Rules shall be determined in accordance with Clause 8 Article 4 of Resolution No. 107/2023/QH15. In Vietnam, Tangible asset carve-out and payroll carve-out under the GloBE rules include the total amount of deductions for tangible assets and the total amount of deductions for payroll of each Constituent Entity, excluding those that qualify as Investment Entities. The method for determining deductions for tangible assets and payroll is set out in Point 6, Section II of Appendix II.

Additional Current Top-up Tax

Additional Current Top-up Tax includes:

Top-up tax incurred from recalculation of the Effective Tax Rate and top-up tax of the previous fiscal year according to Point 9.4, Point 11.1, Point 11.4, Section II, Point 1.4, and Point 9, Section III of Appendix II of Decree 236/2025/ND-CP

Top-up tax incurred under Point 8.5 Section II Appendix II of this Decree, unless the Filing Constituent Entity has elected to apply the provisions under Point 8.6 Section II of Appendix II of Decree 236/2025/ND-CP.

The formula to calculate the Income Inclusion Rule (IIR)

The Ultimate Parent Entity, Partially-Owned Parent Entity, and Intermediate Parent Entity directly or indirectly own an ownership interest in Low-Taxed Constituent Entities located in other jurisdictions under the GloBE rules. At any time during the fiscal year, if a taxpayer directly or indirectly owns an ownership interest in Low-Taxed Constituent Entities located in other jurisdictions under the GloBE rules, the taxpayer shall:

Apply the Income Inclusion Rule (IIR);

Declare and pay a minimum amount of tax under the IIR equal to its allocable share of Top-up Tax under the GloBE rules of these Low-Taxed Constituent Entities for the fiscal year

Unless this Top-up Tax has been paid in another jurisdiction where a Qualified IIR is in effect and prioritized under the GloBE rules on tax collection order.

Under Article 5 Resolution 107/2023/QH15, Jurisdictional Top-up Tax shall be determined in accordance with the following formula.

Article 7 Resolution 236/2025/ND-CP specifies Jurisdictional Top-up Tax in a nation.

Deadline for Declaring and Paying Additional Corporate Income Tax under the Anti-Base Erosion Rules

According to Article 6 of Resolution No. 107/2023/QH15, the declaration and payment of tax shall be carried out as follows:

Regarding the Qualified Domestic Minimum Top-up Tax (QDMTT)

The deadline for submitting the Information Return under the Global Minimum Tax Rules, the Supplementary Corporate Income Tax Return, along with the explanatory statement on differences due to varying financial accounting standards, and the deadline for paying the supplementary corporate income tax, is no later than 12 months after the end of the fiscal year.

Regarding the Income Inclusion Rule:

The deadline for submitting the Information Return under the Global Minimum Tax Rules, the Supplementary Corporate Income Tax Return, along with the explanatory statement on differences due to varying financial accounting standards, and the deadline for paying the supplementary corporate income tax is: No later than 18 months after the end of the fiscal year for the first year in which the multinational enterprise group is subject to the rules; No later than 15 months after the end of the fiscal year for subsequent years.

The above is an update on global anti-tax evasion: new corporate income tax rules in Vietnam. If you have any related questions or need tax legal consultancy, please contact Viet An Law Firm – Tax Agent for the best support and advice.

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

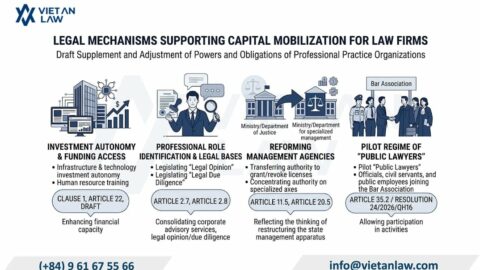

Capital contributing members in law firms Vietnam: Draft Law on Lawyers 2026 allows non-lawyer investors in limited liability law firms for the first time. Effective March 2027.

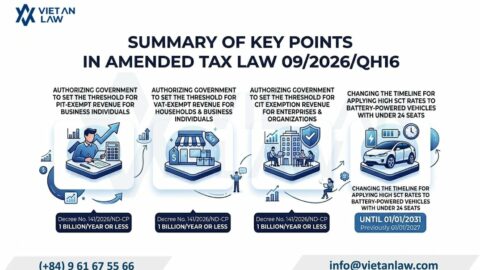

Law 09/2026/QH16 raises tax exemptions to 1 billion VND for household businesses. Learn PIT, VAT, CIT changes 2026 and who benefits most from Vietnam's new tax thresholds.

Is the director's salary single-memeber LLC subject to PIT? Complete 2026 legal analysis on personal income tax, deductible expenses, and compliance rules for LLC directors in Vietnam.

Can AI receive industrial property protection in Vietnam? Learn the legal requirements, significant human contribution criteria, and registration procedures under Decree 100/2026.

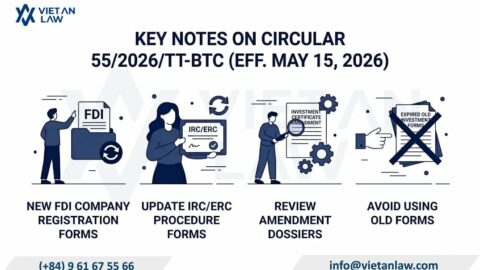

On May 15, 2026, the Ministry of Finance promulgated Circular 55/2026/TT-BTC prescribing the forms of documents and reports related to investment activities in Vietnam and investment promotion. This represents a…