How to account for goods not subject to VAT in Vietnam

Value-added tax is a common tax and needs to be declared and accounted in accordance with the current tax law and accounting law of Vietnam. Immediately, Viet An tax agent will guide the most detailed and accurate accounting of goods not subject to VAT as a basis for making VAT reports according to the declaration period and financial statements at the end of the fiscal year.

Law on Value Added Tax, Law on Excise Tax and Law on Tax Administration amended in 2016

Law Amending Tax Laws 2014

Law on Value-Added Tax amended 2013

Decree 209/2013/ND-CP guiding the Law on Value Added Tax.

Decree 91/2014/ND-CP: Amending and supplementing a number of articles in decrees regulating taxation, issued on 01/10/2014.

Decree 12/2015/ND-CP: Detailing the implementation of the Law amending and supplementing a number of articles of tax laws, promulgated on 12/02/2015.

Decree 100/2016/ND-CP: Detailing and guiding the implementation of a number of articles of the Law on VAT, the Law on Excise Tax and the Law on Tax Administration, promulgated on July 1, 2016.

Decree 146/2017/ND-CP: Amending and supplementing a number of articles of decrees regulating VAT, issued on 15/12/2017.

Decree 49/2022/ND-CP: Amending and supplementing a number of articles of Decree 209/2013/ND-CP, issued on July 29, 2022.

Concept of value-added tax

It is a tax calculated on the added value of goods and services arising in the process from production, circulation to consumption.

Scope of application

Taxpayers

Organizations and individuals producing and trading goods and services subject to VAT.

HH importers and buyers of foreign services are subject to VAT.

Comprise:

Business organizations.

Economic organizations of political organizations and socio-political organizations.

Foreign-invested enterprises.

Individuals, households, and groups of independent business people.

Organizations and individuals engaged in production and business in Vietnam that purchase services (including the case of purchasing services associated with goods) from foreign organizations.

Taxable objects

General principles: Goods and services used for production, business and consumption in Vietnam (including goods and services purchased by overseas organizations and individuals), except for those not subject to VAT.

Subjects not subject to VAT

Essential goods and services – limiting regression

Cultivation and livestock products are not subject to VAT when they are new products that have been preliminarily processed; at the stage of direct cultivation and fishing or importation.

Goods and services belonging to activities eligible for incentives for social and humanitarian purposes are not of a business nature.

Goods and services of some industries are still difficult, and need to be encouraged to facilitate development.

Non-consumer goods and services in Vietnam.

Some services are difficult to determine the added value – efficiency.

Goods and services of business households and individuals with an annual turnover of VND 100 million or less.

Tax deduction principles

Principle 1: Input VAT on goods and services used for production and trading of goods and services subject to VAT shall be fully deducted.

Principle 2: Input VAT arising in any period shall be declared and deducted when determining the payable tax amount of that period, regardless of whether it has been exported or still in storage.

Conditions for input VAT deduction

Have legal invoices and documents in accordance with regulations.

There is a non-cash payment voucher if the purchased goods and services are valued at 20 million VND or more.

For exported goods and services in addition to ensuring the above 2 conditions, there must be other documents:

Contracts for sale, processing of goods and provision of services to foreign organizations and individuals.

The customs declaration has completed customs procedures under the guidance of the Ministry of Finance.

Invoices for sale of goods or services or return of processed goods.

Non-cash payment vouchers.

How to account for goods not subject to VAT

For purchased goods and services

In principle, purchased goods and services that are not subject to VAT will not be deducted from input VAT. Therefore, when accounting, account 1331 (input VAT is deducted) will not be used.

For invoices for purchase of goods, the accountant will account:

Debit 156

Yes 331/111/112

For service purchase vouchers, the accountant will account:

Debit 242/6421/6422

Yes 331/111/112

For goods and services sold

When issuing sales invoices, the accountant will record the revenue by entry:

Debit 131/111/112

Yes 511

Above is some information and instructions on how to account for goods not subject to VAT that Viet An Tax Agent would like to disseminate to readers. Hope this knowledge will help you in the profession!

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

Learn how to reactivate locked tax code Vietnam in 6 fastest steps (2026). Complete guide covers causes, procedures, and common mistakes to restore your tax code quickly.

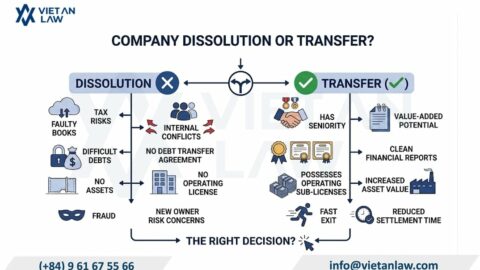

Company dissolution vs transfer in Vietnam: Compare costs, tax obligations, and legal risks. Expert analysis to help you choose the optimal exit strategy for your business.

Inactive company Vietnam? Learn whether to suspend or dissolve your business. Expert guide on legal consequences, procedures, and optimal solutions for non-operating enterprises.

Discover the 6 employment contracts exempt from social insurance Vietnam under the 2024 Social Insurance Law. Learn legal exemptions, compliance risks, and cost optimization strategies for businesses.

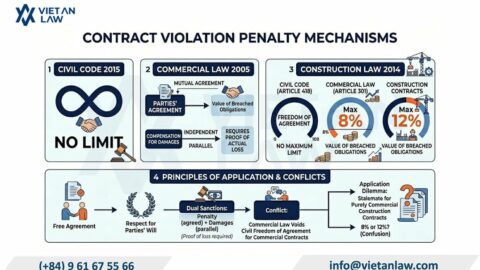

Vietnam's draft Commercial Law 2026 removes the 8% contract penalty cap, allowing unlimited breach penalties. Learn how this affects your contracts, liquidated damages clauses, and dispute strategy.