Regulations on when to issue VAT invoices in Vietnam

In production and business activities, value-added invoices (VAT) are not only important documents for accounting and tax work but also a legal basis for determining financial obligations to the State. One of the key contents that businesses need to comply with is the regulation on the time of issuing VAT invoices. Determining the right time to issue invoices not only helps businesses avoid tax risks, but also contributes to ensuring transparency and legal compliance in the process of commercial transactions. This article of Viet An Tax Agent will help customers learn in detail the current legal regulations on the time of invoicing, as well as the actual situations that businesses often encounter.

Table of contents

Hide

Time of invoicing for the sale of goods in Vietnam

Pursuant to Clause 1, Article 9 of Decree No. 123/2020/ND-CP, amended and supplemented by Decree No. 70/2025/ND-CP (effective from June 1, 2025), the time of issuing value-added invoices for the sale of goods (including the sale and transfer of public assets and the sale of goods subject to national reserve) is determined as the time of transfer of ownership or use rights use the goods to the buyer, regardless of whether the seller has collected the money or not.

For the export of goods (including export processing), the time of issuance of e-commerce invoices, electronic value-added invoices or electronic sales invoices shall be determined by the seller. However, this time must not be later than the next working day from the date the goods are cleared, according to the provisions of customs law.

The time of invoicing the provision of services in Vietnam

According to Clause 2, Article 9 of Decree 123/2020 (amended and supplemented by Decree 70/2025), the time of invoicing for service provision activities is the time of completion of service provision – including the case of providing services to foreign organizations and individuals regardless of whether money has been collected or not.

In case the service provider collects money before or during the performance of the service, the time of invoicing is the time of collection. However, this regulation does not apply to revenues such as deposits or advances to ensure the performance of contracts for the provision of professional services such as: accounting, auditing, financial – tax consulting, price appraisal, survey, technical design, supervision consultancy, etc formulation of construction investment projects.

If goods or services are delivered or handed over many times, according to each item or stage, each delivery or handover must be invoiced corresponding to the actual volume and value performed.

Invoice time for some specific cases

For cases of providing goods and services regularly and in large volumes, it takes time to reconcile data. The time of invoicing is when the data reconciliation between the parties is completed, but no later than the 1st day of the month following the month in which it arises or 07 days after the end of the convention period. The convention period is determined according to the agreement between the seller and the buyer to calculate the quantity of goods and services providedApplicable to fields such as:

Direct support services for air transportation, aviation fuel supply for airlines, power supply

Railway and waterway transport support services; television services, television advertising; e-commerce; post, delivery (including agents, collectors and supporters); telecommunications (including value-added telecommunications).

Logistics and information technology services sold on a certain period; banking services (except for lending activities), international money transfers, securities services, computerized lotteries; collecting road use fees between investors and toll collectors.

Other cases under the guidance of the Ministry of Finance.

Telecommunications and information technology services are connected between service providers. Applicable to telecommunications services (including value-added), information technology services (including payment intermediaries on technology platforms). The time of invoicing is when the reconciliation of service charges under the contract between business establishments is completed, but not later than 2 months from the month in which the connection charges are incurred.

Selling prepaid telecommunications services, collecting network connection charges. If the customer does not request an invoice or does not provide sufficient information (name, address, tax identification number). Business establishments shall issue general VAT invoices at the end of each day or periodically throughout the month, recording the total revenue generated by each type of service.

Construction and installation activities. The time of invoicing is when accepting, handing over the project or the completed volume, regardless of whether the money has been collected or not.

Real estate business, infrastructure construction, building houses for sale or transfer.

Invoice time for real estate business

Retail and food service establishments according to the model of chain stores accounting at the head office: At the end of each day, based on the payment slip and e-invoice to summarize sales transactions and provide services during the day. If the customer requests, the establishment must make and deliver individual e-invoices.

Electricity sales of power generation companies:

E-invoicing is based on the time of reconciliation of payments between the power system operator, the electricity market, the power transmitter and the power purchaser. No later than the last day of the time limit for tax declaration and payment of the month in which tax obligations arise.

If there is a commitment to guarantee from the Government, the time of making invoices shall be according to the contents of the guarantee and guidance of the Ministry of Industry and Trade and the signed power purchase contract.

Selling petrol and oil at retail stores: The time of e-invoicing is right at the end of each sale. The seller is responsible for fully storing e-invoices for business and non-business customers, and at the same time ensuring the ability to look up at the request of the authorities.

Provision of services through agents: The time of invoicing is when the data reconciliation between the parties is completed, but not later than the 10th day of the month following the month in which the service arises.

Lending activities of credit institutions:

Invoice time: It is when the loan interest is collected from the customer according to the term in the credit contract.

If the customer pays the interest before the due date, the invoice is made at the time of receiving the interest before the due date

In case the due date is due but interest is not collected and the loan is monitored off-balance, no invoice shall be made at that time.

Foreign currency transactions of credit institutions: Invoice at the time of performing foreign currency exchange transactions or completing payment services.

Passenger transportation business by taxi: For taxis using payment software, e-invoices are made immediately at the end of the trip and send invoice data to the tax authority as prescribed.

Medical examination and treatment establishments using management software:

If the customer does not request an invoice, the facility prepares a summary invoice at the end of the day based on examination information and receipts.

If the customer requests it, the facility must issue a separate electronic invoice and provide it to the customer.

In the case of health insurance payments, the invoice is issued at the time the Social Insurance Agency settles the costs.

Road use service charge (ETC):

For each turn: The invoice is made on the day the vehicle passes through the toll booth

If the customer has many vehicles used many times in a month, the invoice can be made periodically, no later than the last day of the month in which the service arises. The invoice must list in detail each turn, including: the time the vehicle passes through the station, the fee for each turn.

Insurance business: The time of invoicing is when recording insurance revenue, in accordance with the provisions of the law on insurance business.

Trading traditional lottery tickets, lotteries know the results immediately: After revoking the tickets that are not fully consumed, and before the next prize draw, the enterprise must make an electronic VAT invoice with the tax authority’s code for each agent (organization or individual) who has sold tickets in the period.

Casino and electronic game business with prizes: E-invoices shall be made within 01 day from the end of the date of revenue determination.

If you have any difficulties or questions related to the regulations on the time of issuing VAT invoices, please contact Viet An Tax Agent for the most specific advice.

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

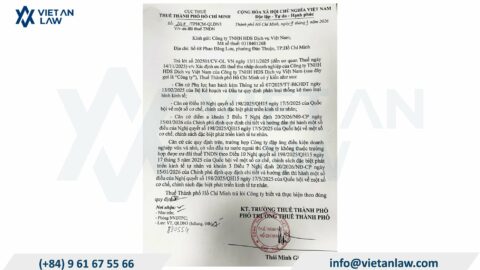

According to Official Letter 2169/TPHCM-QLDN3 (March 2026) issued by the Ho Chi Minh City Tax Department, the regulations on tax incentives under Resolution 198/2025/QH15 and Decree 20/2026/ND-CP have been clarified:…

In the context of rapid digital transformation and the increasing demand for financial transparency, numerous new regulations on non-cash payments are continuously being introduced. These changes directly impact the financial…

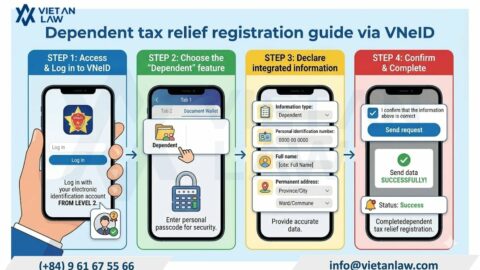

Learn how to register dependent deduction via VNeID in minutes. Step-by-step online guide covering documents, common errors, and 2026 PIT deduction rules. Start now!

Conditions for VAT Refund in Vietnam from July 2025 explained. Discover eligible cases, required documents, and key changes under VAT Law 2024. Contact Viet An Law now!

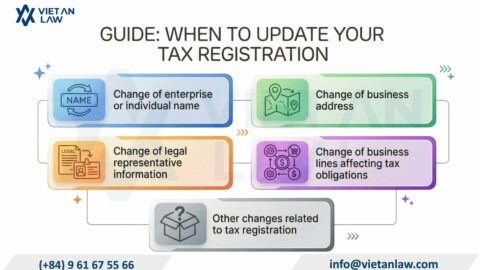

Need to update tax registration information at Ho Chi Minh City Tax Department? Viet An Law guides you through dossiers, procedures & key deadlines. Contact us now!