Regulations on non-deductible interest expenses in Vietnam

In business activities, interest expense is a common and important expense that directly affects the financial results and tax obligations of enterprises. However, not all interest expenses incurred are allowed to be included in deductible expenses when determining taxable income. The current tax law clearly stipulates cases in which loan interest expenses are not deducted in order to avoid enterprises taking advantage of loans to reduce tax obligations unreasonably. The correct understanding and correct application of these regulations not only helps businesses comply with the law but also optimizes the efficiency of financial management, avoiding legal risks in the process of tax declaration and finalization. In this article, Viet An Tax Agent will focus on clarifying the regulations on non-deductible interest expenses, helping businesses grasp and apply them correctly in practice.

Table of contents

Hide

Concept of interest expense

Interest Expense is an expense incurred when an enterprise or individual borrows capital from organizations such as banks, credit institutions or from other individuals to serve production, business activities or other purposes, and must pay interest on that loan. This is an important financial expense, recorded on the enterprise’s financial statements and may directly affect the determination of income subject to corporate income tax if it fully meets the conditions prescribed by law.

Pursuant to Clause 3, Article 113 of Circular 200/2014/TT-BTC, interest expense is specifically defined as follows: This is the interest expense incurred in the reporting period, which is included in the financial expense of the enterprise. The data recorded is based on the detailed accounting books of Account 635. Note that the interest expense reflects the amount of interest incurred in the period, not the amount of interest payable in that period.

Characteristics of interest expense

Interest expense is a periodic financial expense arising from the use of loan capital, which is specific in nature and closely depends on the loan contract as well as legal provisions related to interest rates, capital use purposes and tax deduction conditions. The outstanding characteristics of interest expense are shown as follows:

Recorded in production and business expenses: Interest expenses shall be accounted into production and business expenses as soon as they are incurred, unless these expenses are capitalized according to the provisions of Vietnam Accounting Standard No. 16. Capitalization helps accurately reflect the costs associated with fixed assets, thereby improving transparency in financial statements.

Essentially financial expenses: This is an expense arising from borrowing, which is reflected on the financial statements of the enterprise, usually included in the financial expenses section of the statement of business results, showing the financial burden of the enterprise in the reporting period.

Depends on the loan contract: The interest expense is determined based on the terms of interest rate and term stated in the loan contract. Interest rates can be fixed or floating, depending on the agreement between the borrower and lender, and are affected by market volatility and monetary policy.

Direct impact on cash flow and profit: Interest expense reduces the pre-tax profit of the business, thereby impacting profitability and overall financial situation. This is also an important factor to assess debt repayment capacity and the efficiency of using loans in production and business activities.

Depends on the general interest rate of the market: When inflation rises, market interest rates often tend to increase, leading to an increase in interest costs of businesses. On the contrary, in the context of declining inflation, interest costs also tend to go down, contributing to improving the financial situation of enterprises.

Regulations on interest expenses when calculating CIT

Pursuant to Clause 2, Article 4 of Circular 96/2015/TT-BTC, interest expenses that are allowed to be included in deductible expenses when determining corporate income tax include:

The interest expense arising from borrowing capital for production and business of entities other than credit institutions or economic organizations, if it exceeds 150% of the basic interest rate announced by the State Bank of Vietnam at the time of borrowing, the excess will not be included in the deductible expenses.

The cost of interest payment corresponding to the charter capital of the private enterprise (considered as investment capital) has not been fully contributed according to the capital contribution schedule stated in the enterprise’s charter, even if the enterprise has been put into production and business activities. Interest expenses in the investment process that have been capitalized into the value of assets or investment works are not excluded. In case the enterprise has fully contributed charter capital, if there is a loan interest payment to invest in another enterprise, this expense shall be included in the deductible expenses when determining taxable income.

Regarding the cost of paying loan interest corresponding to the missing charter capital according to the capital contribution schedule, the non-deductible expenses are determined as follows:

If the loan amount is less than or equal to the missing charter capital, the entire loan interest expense is an expense that cannot be deducted.

If the loan amount is greater than the missing charter capital:

In addition, according to Clause 3, Article 16 of Decree 132/2020/ND-CP, interest expenses incurred in transactions with associated parties are included in deductible expenses if the following conditions are satisfied:

The total interest expense after deducting deposit interest and loan interest incurred in the period must not exceed 30% of the total net profit from business activities arising in the tax period.

The interest expense that is not deducted due to excess will be carried forward to the next tax period to be calculated together with the total interest expense deducted in the new period, in order to ensure reasonable cost optimization for the enterprise.

Regulations on non-deductible interest expenses when calculating CIT

Unreasonable interest expenses are expenses arising from borrowing activities but do not meet the conditions prescribed by Vietnamese law to be included in deductible expenses when determining income subject to corporate income tax. These expenses not only affect the determination of taxable profits but can also lead to legal risks for businesses if not handled properly.

Specifically, interest expenses that are considered unreasonable include but are not limited to the following cases:

Interest rates exceeding the permissible limit: Interest expenses arising from loans with interest rates exceeding 150% of the basic interest rate announced by the State Bank of Vietnam at the time of borrowing. Interest expenses in excess of this level will not be recognized as deductible expenses for tax purposes.

Interest expenses corresponding to the insufficient contributed charter capital: Loan interests incurred corresponding to the amount of charter capital that the enterprise has not contributed according to the schedule registered in the enterprise charter are also excluded. This is to limit the borrowing of capital for use by enterprises instead of contributing equity.

Capitalized interest expenses: Interest expenses that have been capitalized into the value of fixed assets or investment works as prescribed by accounting standards shall not be re-included in expenses when determining taxable income in order to avoid duplicate calculation of expenses

Interest expenses arising from illegal loans: Including loans that do not have a legal loan contract, do not have full payment documents or do not comply with regulations on loan procedures according to current laws.

Interest expenses that do not serve production and business purposes: Loan interests that are not directly related to the production and business activities of the enterprise, such as loans for personal purposes or investments not related to business activities, will not be included in reasonable expenses.

Interest expense exceeds the limit of 30% of net profit from business activities in the period: According to the provisions of Decree 132/2020/ND-CP, the total interest expense (after deducting deposit interest and loan interest incurred in the period) must not exceed 30% of net profit from business activities arising in the tax period. This excess cost will not be deducted and will be carried forward to the next period for further calculation.

Clearly distinguishing and complying with regulations on reasonable interest expenses helps businesses ensure accurate tax declaration, avoid being sanctioned for tax law violations and at the same time optimize the efficiency of financial management in business activities.

Deductible interest expense when calculating CIT for enterprises with related-party transactions

According to Clause 3, Article 16 of Decree 132/2020/ND-CP, deductible loan interest expenses when determining income subject to corporate income tax for enterprises with related-party transactions are prescribed as follows:

Interest expense deduction limit: The total interest expense (after deducting deposit interest and loan interest incurred in the period) is deducted not exceeding 30% of total EBITDA in the tax period, including:

Net profit from business activities

Net interest expense (net deposit interest and loan interest)

Fixed asset depreciation costs

The expense in excess of 30% will not be deducted immediately, but can be carried forward to the next tax period (if the interest rate deducted in the next period is lower than the allowable level). The maximum transfer period shall not exceed 5 consecutive years, counting from the year following the year in which interest expenses are incurred shall not be deducted.

Loans that are not subject to the 30% limit include:

Borrowing from credit institutions under the Law on Credit Institutions

Borrowing from insurance business enterprises under the Law on Insurance Business

ODA loans, concessional loans of the Government by the method of on-lending

Loans for national target programs such as new countryside, sustainable poverty reduction

Loans for social policy projects: resettlement housing, worker housing, student housing, social housing and other public welfare works

Enterprises with related-party transactions are responsible for declaring the interest expense ratio in the period according to Appendix I issued together with Decree 20/2025/ND-CP.

If you have any difficulties or questions related to the regulations on interest expenses that are not deductible, please contact Viet An Tax Agent for the most specific advice.

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

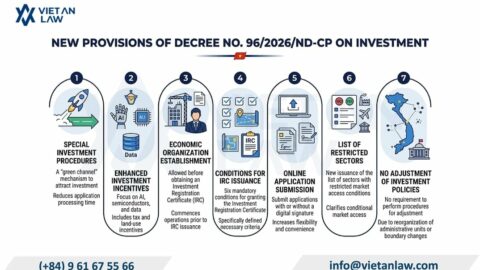

Decree 96/2026/ND-CP Guiding the Vietnam Investment Law 2025 introduces special investment procedures, new incentives for AI and semiconductors, and streamlined processes effective March 31, 2026.

Latest Updates on Tax Administration for Associated Transactions in Vietnam 2026. Complete guide covering transfer pricing, CbCR requirements, and compliance obligations.

Enterprise Formation & Registration Services in Binh Duong, HCMC. Expert guidance on company setup, legal compliance, tax incentives, and FDI procedures. Contact us today!

Effective from March 1, 2026, the Law on Restructuring and Bankruptcy 2025 will officially come into force, replacing the Law on Bankruptcy 2014. This law marks a significant development in…

Vietnam LLC Formation guide: Complete post-incorporation procedures after obtaining your ERC. Learn required steps including board meetings, signage, bank accounts, and tax registration for compliance.