In the context of national digital transformation, the integration of national ID with tax codes in Vietnam: Benefits and new regulations from July 1, 2025, according to Decision 06/QD-TTg/2022 on the Project on developing applications of data on population, identification, and electronic authentication marks an important step in administrative procedure reform. Viet An Law provides professional tax and corporate legal consulting services, supporting clients to effectively comply with new regulations and make the most of the practical benefits that the policy brings to both individuals and enterprises.

Table of contents

Hide

Time to apply new tax code regulations

Current tax codes issued by tax authorities to individuals, households, and business households are valid until June 30, 2025 (Clause 2, Article 38, Circular 86/2024/TT-BTC);

From July 1, 2025, taxpayers, tax authorities, other agencies, organizations, and individuals related to the use of tax codes as prescribed in Article 35 of the Law on Tax Administration 2019, amended and supplemented in 2024, shall use national ID instead of tax codes;

From February 6, 2025, the national ID will begin to be used to replace tax codes for individuals, households, and business households.

Timeline for applying the regulation on integrating national ID with tax codes in Vietnam

Minimize administrative procedures for individuals

Synchronizing national ID with personal tax codes helps reduce and simplify tax-related administrative procedures, specifically:

Simplify the tax registration process

Under the new regulations, the national ID replacing the tax code brings significant convenience in tax registration. According to the Tax Department’s guidance on using the replacement identification number in cases where taxpayers have not been granted a tax code before July 1, 2025:

When registering a new tax code, taxpayers only need to accurately declare 03 basic information: full name, date of birth, and national ID;

There is no need to submit a copy of the citizen identification card to the tax authority because the data has been synchronized with the National Population Database.

File processing time is shortened thanks to automatic information comparison.

For Tax Codes issued before July 1, 2025:

In case the tax registration information is correct, the tax authority will convert it to a national ID, and no administrative procedures will arise for the taxpayer when converting.

In case the information does not match, the Tax Authority will update the tax code status to status 10 “MST waiting for updating national ID information”. Taxpayers must carry out procedures to change tax registration information with the tax authority according to the provisions of Clause 1, Clause 4, Article 25 of Circular 86/2024/TT-BTC.

Optimize tax lookup and fulfillment.

Pursuant to Article 41 of the Law on Tax Administration 2019, the use of a national ID helps:

People do not need to remember separate tax codes; they only need to use a single identification code.

Tax information lookup becomes faster and more accurate;

Conduct electronic tax transactions conveniently.

Improve management efficiency for enterprises.

Save time and operating costs.

For the enterprise sector, national ID replaces tax codes: Benefits and new regulations from July 1, 2025, create specific benefits:

Reduce data entry time and compare personal information when performing authorized tax registration;

Simplify the personal income tax declaration process for employees;

Automate the updating of employee information through connection to the national database.

Increase accuracy in tax declaration.

According to Circular 86/2024/TT-BTC, enterprises benefit from:

Data synchronization helps reduce errors in declaration.

Automatically update changes in personal information from the central database;

Improve the efficiency of tax liability implementation for employees.

Legal regulations and procedures for changing information

Legal basis for conversion

The integration of the national ID with tax codes in Vietnam, from July 1, 2025, is based on the following legal documents:

Law on Tax Administration 2019, especially Article 41 on changes to tax registration information;

Decision 06/QD-TTg/2022 on the Project on developing population data applications for the period 2022-2025;

Circular 86/2024/TT-BTC providing detailed guidance on tax registration (replacing the old Circular 105/2020/TT-BTC).

Procedures for updating tax registration information

According to Article 26 of Circular 86/2024/TT-BTC, the processing procedures are classified as follows:

For changes to information not on the Tax Registration Certificate:

Processing time: 02 working days from the date of receiving complete documents;

Tax authorities update information in the Tax Registration Application System.

For changes to information on the Tax Registration Certificate:

Processing time: 03 working days;

Issue Certificate or Notice of updated tax code.

Procedures for updating tax registration information

Benefits of national data synchronization

Integration with the National Population Database

National ID replacing tax code applied from July 1, 2025, contributes to building a unified national information system under a single code:

Seamless connection between state agencies;

Minimize data duplication and improve accuracy;

Create the premise for comprehensive digital transformation in state management.

Enhance transparency and accountability.

Using a unique national ID across the tax system helps:

Enhance the ability to trace and monitor tax activities;

Prevent the theft of personal tax codes as has happened in the past;

Improve the efficiency of tax inspection and examination;

Ensure fairness in tax obligations.

Procedures for changing location and updating information

Procedures for business households and individual businesses

According to Article 25 of Circular 86/2024/TT-BTC, changes to tax registration information are made as follows:

At the tax authority of the former location:

Processing time: 05 working days (in case of inspection) or 07 working days (in case of no inspection);

Conditions: Taxpayers have fulfilled their obligations under Decree 126/2020/ND-CP;

Issue a Notice of change of location according to form 09-MST.

At the tax authority of the new location:

Processing time: 03 working days from the date of receiving complete documents;

Update information in the Tax Registration Application System;

Issue a new Tax identification number certificate or Notice.

Special cases and exception handling

For cases where taxpayers have not fulfilled their obligations at the tax authority where they move:

The time limit for issuing the Notice is adjusted to 03 working days from the date of completion of the obligation;

Apply the same provisions as Clause 3, Article 11 of Circular 86/2024/TT-BTC for cases where the application for change of address has not been submitted.

Instructions and important notes

Prepare for the transition

To optimize the application of national ID instead of tax codes according to new regulations from July 1, 2025, organizations and individuals need to:

Update citizen identification information in tax registration dossier;

Ensure personal information matches exactly with the National Population Database;

Follow specific instructions from tax authorities on the conversion process.

The role of professional consulting services

During this transition, enterprises should:

Consult with reputable legal consulting organizations;

Ensure full compliance with new legal regulations;

Develop internal procedures in line with new requirements.

The transition to using personal identification numbers is not only a mandatory requirement but also an opportunity to improve management efficiency and reduce compliance costs. We recommend that enterprises and individuals proactively prepare and implement early to ensure the transition is smooth and most effective. This is an important step in the modernization of Vietnam’s tax management system. This change not only brings practical benefits to both individuals and enterprises but also contributes to building an effective and transparent public administration.

At Viet An Law, with a team of experienced experts, we are committed to providing comprehensive consulting services on integrating national ID with tax codes in Vietnam from July 1, 2025, helping customers optimize compliance processes and maximize benefits from the new regulations. Please contact us for the most timely advice!

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

According to Official Letter 2169/TPHCM-QLDN3 (March 2026) issued by the Ho Chi Minh City Tax Department, the regulations on tax incentives under Resolution 198/2025/QH15 and Decree 20/2026/ND-CP have been clarified:…

In the context of rapid digital transformation and the increasing demand for financial transparency, numerous new regulations on non-cash payments are continuously being introduced. These changes directly impact the financial…

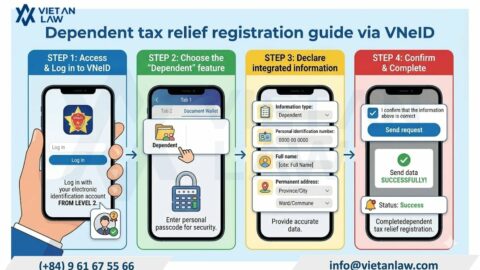

Learn how to register dependent deduction via VNeID in minutes. Step-by-step online guide covering documents, common errors, and 2026 PIT deduction rules. Start now!

Conditions for VAT Refund in Vietnam from July 2025 explained. Discover eligible cases, required documents, and key changes under VAT Law 2024. Contact Viet An Law now!