E-Invoices from Cash Registers in Vietnam from 2025

The year 2025 marks a major turning point in tax administration in Vietnam, especially with the introduction and practical enforcement of regulations on e-invoices from cash registers in Vietnam from 2025. This is not only an administrative reform but also a modern technological solution aimed at optimizing tax collection procedures, enhancing transparency, and preventing tax fraud.The implementation of e-invoices from cash registers in Vietnam from 2025 is expected to deliver substantial benefits for both tax authorities and the business community, particularly enterprises and household businesses in the retail and service sectors.This article provides a detailed analysis of the core regulations, applicable subjects, implementation procedures, and key considerations to ensure that organizations and individuals can effectively apply e-invoices from cash registers in Vietnam from 2025, contributing to the development of a fairer and more modern tax system.

Table of contents

Hide

Definition of E-Invoices from Cash Registers in Vietnam from 2025

According to Point c, Clause 2, Article 3 of Decree No. 123/2020/ND-CP, as amended and supplemented by Point a, Clause 2, Article 1 of Decree No. 70/2025/ND-CP, e-invoices from cash registers in Vietnam from 2025 are defined as follows:

E-invoices from cash registers (or e-invoices from cash registers with electronic data connection to tax authorities) are invoices with a tax authority code or electronic data allowing buyers to access and declare information. These invoices are generated by organizations or individuals selling goods and providing services through a cash register system. The data is electronically transmitted to the tax authority in a standardized format.

Mandatory Use Cases of E-Invoices from Cash Registers in Vietnam from 2025

Pursuant to Clause 1, Article 11 of Decree No. 123/2020/ND-CP, as amended by Clause 8, Article 1 of Decree No. 70/2025/ND-CP, from June 1, 2025, the following five cases are required to use e-invoices from cash registers in Vietnam from 2025:

Household businesses and individual business households with annual revenue of VND 1 billion or more (as stipulated in Clause 1, Article 51; Clause 2, Article 90; and Clause 3, Article 91 of the Law on Tax Administration 2019).

Enterprises engaged in the sale of goods or provision of services, including commercial centers, supermarkets, and retail stores (excluding automobiles, motorcycles, motorbikes, and other motor vehicles).

Restaurants, catering businesses, and hotels.

Passenger transportation services and directly related road transport support services.

Art, entertainment, cinema activities, and other personal service providers.

Principles for Applying E-Invoices from Cash Registers in Vietnam from 2025

According to Article 11 of Decree No. 123/2020/ND-CP, amended and supplemented by Clause 9, Article 1 of Decree No. 70/2025/ND-CP, the following principles govern the use of E-Invoices from Cash Registers in Vietnam from 2025:

First, businesses must ensure that the invoice printed from the cash register is electronically transmitted to the tax authority and can be identified as such.

Second, the use of digital signatures is not mandatory for businesses applying E-Invoices from Cash Registers in Vietnam from 2025.

Third, expenses for purchasing goods or services using E-Invoices from Cash Registers in Vietnam from 2025 are considered legitimate deductible expenses for tax purposes, provided that either a photocopy of the invoice or information retrieved from the General Department of Taxation’s e-Portal is available.

Content Requirements for E-Invoices from Cash Registers in Vietnam from 2025

According to Article 10 of Decree No. 123/2020/ND-CP as amended by Clause 8, Article 1 of Decree No. 70/2025/ND-CP, E-Invoices from Cash Registers in Vietnam from 2025 must include the following contents:

Name, address, and tax identification number (TIN) of the seller;

Name, address, tax identification number/personal identification number/phone number of the buyer (if requested by the buyer);

Date and time of invoice issuance;

Description of goods or services, unit price, quantity, and total amount payable;

Tax authority’s code or electronic data that allows the buyer to retrieve and declare the information on the e-invoice from the cash register;

The seller shall deliver the e-invoice to the buyer via electronic means (such as SMS, email, or other methods), or provide a URL or QR code for the buyer to access and download the e-invoice.

Delivery of E-Invoices from Cash Registers in Vietnam from 2025 to Buyers

According to the new regulation under Article 22 of Decree No. 70/2025/NĐ-CP, sellers are required to deliver e-invoices to buyers through electronic means, specifically as follows:

Via text message (SMS);

Via email;

Through other electronic methods, or by providing a URL or QR code for the buyer to access and download the e-invoice.

Responsibilities of Tax Authorities for E-Invoices Generated from Cash Registers

Clauses 39 and 40, Article 1 of Decree No. 70/2025/NĐ-CP stipulate the responsibilities of tax authorities for e-invoices generated from cash registers as follows:

The tax authorities, in coordination with local People’s Committees, are responsible for reviewing, classifying, and implementing measures to encourage taxpayers to adopt e-invoices generated from cash registers.

In cases where organizations, business households, or individual businesspersons are required to use e-invoices generated from cash registers but lack the necessary IT infrastructure or invoicing systems, tax authorities must develop support plans and notify taxpayers to facilitate the transition to e-invoices generated from cash registers.

If a taxpayer, after receiving support and notification from the tax authority, still fails to adopt e-invoices generated from cash registers, it will be considered a violation of invoice usage regulations. The tax authority shall report such violations to the People’s Committee for direction and coordination with relevant local agencies to handle violations related to failure to issue invoices and business registration in accordance with tax and invoice laws.

Key Considerations for Applying E-Invoices from Cash Registers in Vietnam from 2025

Review and determine whether your enterprise or business household falls under the mandatory application of e-invoices generated from cash registers as stipulated in Decree No. 70/2025/NĐ-CP.

Prepare the necessary systems and software to ensure that your cash register/POS systems and sales management software can meet the technical requirements for e-invoices and are capable of connecting to the tax authority’s system.

Research and choose a reputable software/system provider that ensures both legal compliance and technical reliability.

Provide training for staff on the procedures for generating, issuing, and handling e-invoices from cash registers.

The above is the legal update from Viet An Law on the regulations regarding e-invoices from cash registers in Vietnam.If you require further legal advice or assistance on how to implement E-Invoices from Cash Registers in Vietnam, please contact Viet An Law for professional support.

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

According to Official Letter 2169/TPHCM-QLDN3 (March 2026) issued by the Ho Chi Minh City Tax Department, the regulations on tax incentives under Resolution 198/2025/QH15 and Decree 20/2026/ND-CP have been clarified:…

In the context of rapid digital transformation and the increasing demand for financial transparency, numerous new regulations on non-cash payments are continuously being introduced. These changes directly impact the financial…

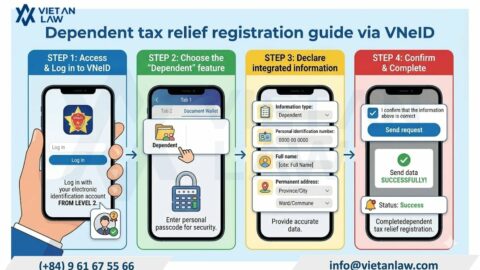

Learn how to register dependent deduction via VNeID in minutes. Step-by-step online guide covering documents, common errors, and 2026 PIT deduction rules. Start now!

Conditions for VAT Refund in Vietnam from July 2025 explained. Discover eligible cases, required documents, and key changes under VAT Law 2024. Contact Viet An Law now!