Instructions on procedures after setting up a company in Poland

When your company is officially incorporated and recorded in the Polish National Register (KRS), the procedure is completed in the first step. In order for the business to be operational, you need to carry out a number of post-establishment procedures. Viet An Law would like to introduce some procedures after establishing a company you need to carry out in Poland through the article below.

Instructions on procedures for opening a bank account after setting up a company in Poland

After the company is incorporated, one of the procedures after setitng up a company is to open a bank account of the company. Poland has a diverse banking system, including local banks and international bank branches.

The list of documents to be prepared includes:

Company registration certificate;

The company’s charter;

Decision on appointment of members of the Management Board;

Identity card or passport of the legal representative;

Instructions on tax registration procedures after setting up a company in Poland

Once your company has been officially established, one of the next important legal tasks is to register for taxes and comply with tax obligations under Polish law. This ensures that your business is carried out legally and avoids tax-related risks. Here are the main aspects you need to keep in mind:

Registration of Tax Identification Number (NIP)

Immediately after incorporation, you need to register to be issued a Tax Identification Number (NIP), a unique number to identify the company in transactions with tax authorities. The NIP registration procedure is relatively simple and needs to be done as soon as the company is officially registered. You will need to fill out the NIP application form and submit it at the local tax office (Urząd Skarbowy) where your company is based.

Register for Value Added Tax (VAT)

If your business involves the sale of goods or the provision of services subject to VAT in accordance with Polish law, you will need to register for VAT. Polish law stipulates a certain revenue threshold that when businesses pass within a certain period of time, they are required to register for VAT. However, even if you haven’t reached the required threshold, you can still choose to register for VAT so that you can deduct input VAT (VAT paid on goods and services you purchase). The types of VAT to register for include domestic VAT for the sale and purchase of goods and services within the territory of Poland and European VAT (EU VAT) if your company has cross-border trade with EU member states, you may need to register for EU VAT to comply with VAT regulations in international transactions.

Instructions on procedures for declaring basic tax information after setting up a company in Poland

NIP-8 Declaration Process

Timing: A NIP-8 return is usually required to be filed within a certain period of time after the company is registered and receives the NIP number.

Declaration form: You will need to fill out an official NIP-8 declaration form, which is provided by the Polish tax authorities.

Information to provide: The NIP-8 declaration requires the provision of detailed information about the business, including:

Full name and initials of the company.

Official registration address.

Contact information (phone number, email).

Main types of business activities.

Information about the legal representative of the company.

Other tax information on request.

Submit the return: The NIP-8 return after filling in all the information needs to be submitted to the local tax authority (Urząd Skarbowy) where your company is headquartered.

Instructions on declaration of civil transaction tax after setting up a company in Poland

The Civil Transaction Tax (Podatek od czynności cywilnoprawnych – PCC) is a tax that applies to certain civil transactions carried out in Poland. For businesses, it is important to understand which transactions are subject to PCC tax and to carry out the relevant declaration and payment procedures to ensure compliance with the law.

Transactions that are generally subject to PCC tax

Not all civil transactions are subject to PCC tax. However, some common transactions that businesses often encounter and may be subject to this tax include:

Property purchase and sale contracts: Including the purchase and sale of real estate (land, houses, apartments), means of transport (cars, motorcycles), and other tangible assets.

Loan contracts: Loan contracts (including intercompany loans) are generally subject to PCC tax.

Company capital contribution contracts: Cash or asset capital contribution to a company may be subject to PCC tax, depending on the type of company and specific regulations.

Other transactions: Certain other civil transactions regulated in Polish law may also be subject to PCC tax.

Tax rate

The PCC tax rate varies depending on the type of transaction. Some common tax rates include:

5%: Applicable to some types of asset purchase and sale contracts and loan contracts.

1%: Applicable to some other types of asset purchase and sale contracts.

2%: Applies to some other transactions.

PCC-3 Declaration and Payment Process

Determine tax liability: Determine whether the transaction you make is subject to PCC tax based on the provisions of the law.

Calculate the tax amount: Calculate the amount of PCC tax payable based on the value of the transaction and the applicable tax rate.

Fill out the PCC-3 form: You need to fill out a tax return form called PCC-3.

Submit a PCC-3 return: The PCC-3 return must be filed with the local tax authority (Urząd Skarbowy) where your company is headquartered.

Tax payment: At the same time as filing the return, you must pay the calculated PCC tax amount.

Deadline: The deadline for filing a PCC-3 return and paying taxes is usually 14 days from the date the tax obligation arises (e.g., the date the contract is signed). However, the specific deadline may vary depending on the type of transaction and legal regulations.

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

Can you dissolve a company with a locked tax code in Vietnam? No—but dissolution is possible after restoring tax compliance. Learn the legal requirements, costs, timeline, and step-by-step procedures to…

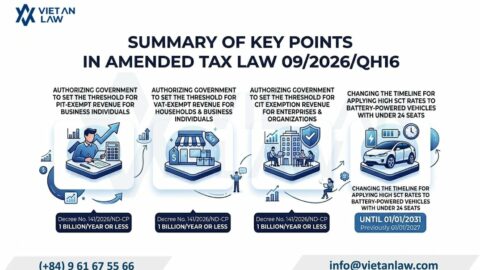

Law 09/2026/QH16 raises tax exemptions to 1 billion VND for household businesses. Learn PIT, VAT, CIT changes 2026 and who benefits most from Vietnam's new tax thresholds.

Complete guide to company branch registration in Hanoi 2026: requirements, procedures, costs, and address selection. Expert legal support for Vietnamese and foreign enterprises establishing branches in Vietnam.

Is the director's salary single-memeber LLC subject to PIT? Complete 2026 legal analysis on personal income tax, deductible expenses, and compliance rules for LLC directors in Vietnam.

PIT Tax Rules for Lunch & Mid-Shift Meals in Vietnam explained. Learn how to calculate personal income tax on meal allowances under 2025 regulations and Official Dispatch 5106.