Preferential Tax Policies for Businesses in Vietnam 2025

In 2025, to facilitate businesses in overcoming difficulties, promoting innovation, and enhancing competitiveness, the Government issued Resolution 198/2025/QH15, stipulating numerous preferential tax policies effective from June 1, 2025. This Resolution, concerning preferential tax policies, plays a crucial role in promoting the development of businesses, especially new, innovative startups and small and medium-sized enterprises (SMEs). In the article below, Viet An Law will analyze the Preferential Tax Policies for Businesses in Vietnam 2025.

Contents of Preferential Tax Policies for Businesses in Vietnam 2025 under Resolution 198/2025/QH15

Before Resolution 198/2025/QH15 takes effect from June 1, 2025, newly established businesses were not entitled to corporate income tax (CIT) policies under current law. Instead, these businesses had to fulfill their CIT obligations according to the general provisions of the CIT Law and guiding documents. After the issuance of the Resolution, preferential tax policies for businesses in Vietnam 2025 have been expanded, creating more favorable conditions for businesses. Specifically:

Exemption of corporate income tax (CIT) for 02 consecutive years

Application conditions:

Businesses newly established from May 17, 2025, onwards

Innovative startup activities of startups

Small and medium-sized enterprises (SMEs).

Policy content: Businesses are exempt from CIT for 02 consecutive years from the start of legitimate production and business activities.

50% reduction in the tax payable for the next 04 years

Application conditions: Newly established businesses, operating in innovative startup activities of startups, small and medium-sized enterprises (SMEs).

Reduction period: 04 consecutive years after the tax exemption period ends.

Policy content: Businesses only need to pay 50% of the CIT for the subsequent 04 years of operation after the exemption period.

Support for fees, charges, and business registration procedures

Application conditions:

Newly established within the specified period (from May 17, 2025)

Operating in innovative startup activities of startups, small and medium-sized enterprises (SMEs)

Not subject to administrative penalties or other legal sanctions.

Fully fulfilling obligations regarding taxes, insurance, and other legal obligations.

Policy content: Businesses are exempted from or receive reductions in fees and charges during the registration, licensing, and certification processes related to business operations.

Support for loans and preferential credit

Application conditions: Businesses must meet criteria regarding financial capacity, feasible projects, and suitability for priority, innovative, and SME sectors.

Policy content: Businesses receive support for loan policies and preferential credit for startups, and small and medium-sized enterprises, to enhance access to capital. Businesses can borrow at interest rates lower than market rates, potentially 30-50% lower than normal loan interest rates. Commercial banks, credit institutions, enterprise development funds, public investment funds, or other financial organizations will dedicate a portion of their capital to preferential lending.

Support for workspace and infrastructure

Application conditions: Businesses newly established from May 17, 2025, onwards, operating in priority, innovative, and SME sectors; having projects or activities consistent with the development goals of supported areas; fully complying with procedures and documentation as stipulated by state management agencies and local authorities.

Policy content: Businesses receive preferential policies for renting premises and infrastructure, creating favorable conditions for business development.

Preferential policies for personal income tax (PIT) and other taxes for employees

Application conditions: Employees working in newly established businesses from May 17, 2025, onwards, having appropriate labor contracts, and being eligible for preferential policies as stipulated by law.

Policy content: Exemption or reduction of PIT for employees working in newly established businesses, especially in priority sectors, innovative startups, and small and medium-sized enterprises.

Reduction period: May extend for the duration that the business enjoys CIT preferential policies, aiming to create favorable conditions for both employees and businesses.

Benefits of Preferential Tax Policies for Businesses in Vietnam 2025

The preferential tax policies applicable to businesses in 2025 bring many practical benefits aimed at promoting the sustainable development of businesses, especially new, innovative startups, and small and medium-sized enterprises.

Fostering startups and innovation

Tax exemptions and reductions in the initial phase help new businesses, especially innovative and high-tech enterprises, develop sustainably, and minimize initial financial risks, thereby promoting innovative activities and enhancing national competitiveness.

Supporting the sustainable development of SMEs

Preferential tax policies help SMEs reduce their financial burden, create conditions for expanding scale, improve competitiveness, and contributing to local and national economic development.

Increasing domestic and foreign investment attraction

Preferential tax, fee, and charge policies create a more attractive and competitive investment environment, attracting domestic and foreign investors and businesses to expand their operations, and contributing to economic growth.

Forming an innovative business ecosystem

Tax support policies, workspace, and preferential credit contribute to building an innovative business ecosystem, promoting innovation centers, research and development, and enhancing global competitiveness.

Contributing to enhancing national competitiveness

These policies help businesses reduce costs, and improve operational efficiency, thereby enhancing the competitiveness of the economy, contributing to achieving sustainable development goals and modernizing the country.

Creating momentum for sustainable, inclusive economic development

Preferential tax policies demonstrate the State’s attention to business development, contributing to building a healthy business environment, promoting inclusive economic development, and reducing inequality.

Businesses effectively leveraging these policies will contribute to creating a favorable business environment, promoting comprehensive and sustainable development in 2025. Above is the advice of Viet An Law on the issue of Preferential Tax Policies for Businesses in Vietnam 2025. Clients who have related questions or need legal support, please contact Viet An Law Firm for the best support!

Fast & Reliable Legal Assistance

Fill out the form below and get connected with a lawyer quickly.

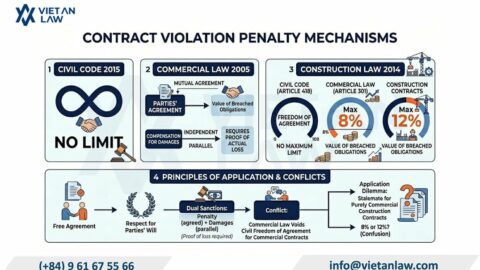

Vietnam's draft Commercial Law 2026 removes the 8% contract penalty cap, allowing unlimited breach penalties. Learn how this affects your contracts, liquidated damages clauses, and dispute strategy.

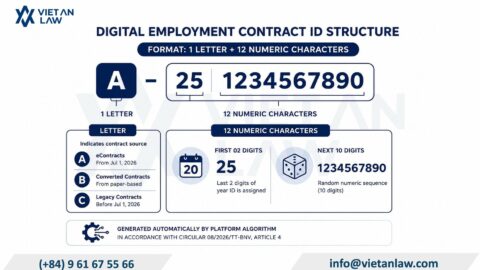

Electronic employment contract Vietnam: Complete guide to Circular 08/2026/TT-BNV key updates on ID codes, eContract platform access, and digital labor contract requirements effective July 2026.

Complete guide to drafting a Non-Disclosure Agreement (NDA) in Vietnam 2026. Learn essential clauses, common mistakes, legal requirements & professional NDA drafting services for businesses.

Can you dissolve a company with a locked tax code in Vietnam? No—but dissolution is possible after restoring tax compliance. Learn the legal requirements, costs, timeline, and step-by-step procedures to…

Capital contributing members in law firms Vietnam: Draft Law on Lawyers 2026 allows non-lawyer investors in limited liability law firms for the first time. Effective March 2027.